by Neil Azous, Chief Investment Officer

- The Starting Point

- Observing The Trend Change

- Confirming an Intermediate-term Trend Change

- Linkage Between NASDAQ-100 & 30-Year US Treasury Yields

- How Much Time Is Left in Interest Rates Rising?

- Investment Implications

The world’s first and second most liquid and important stock indices are the S&P 500 (SPX) and the NASDAQ-100 (NDX).

Structurally, we believe a reversal in the ratio of long NDX versus short SPX (i.e., NDX/SPX) poses the most impending danger to an equity portfolio. The ratio is in the process of confirming an intermediate-term trend change.

Based on the sensitivity of high-multiple stocks in the NDX to longer-dated U.S. Treasuries, the catalyst for the NDX/SPX ratio to fall further is higher 30-year interest rates over the next 6-9 months.

Concurrently, capturing this rotation at the sector and security level may provide a significant opportunity to generate alpha.

The Starting Point

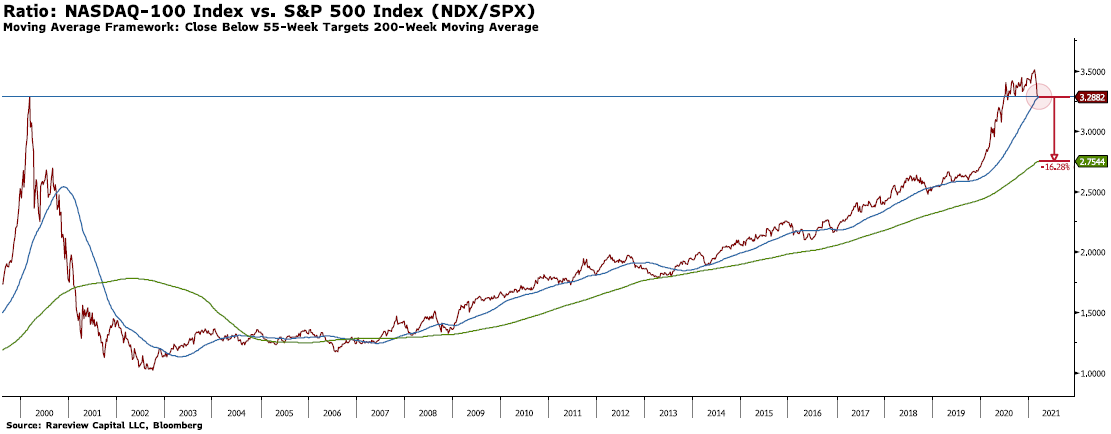

Below is the “weekly” ratio chart of long NDX versus short SPX (NDX/SPX) since 1999.

On March 19, 2000, the NDX/SPX ratio peaked at 3.2881, the highest weekly close ever at the time.

This level of NDX relative outperformance was not reached again until July 2020. Since July 2020, the ratio has settled above 3.2881 on 36 of 38 “weekly” closes. The only exceptions are the July 24, 2020 close at 3.2600 and the March 12, 2021 close at 3.2808.

On March 19, 2021, the NDX/SPX ratio closed at 3.2882 or 0.0001 above the 2000 peak.

Observing The Trend Change

This is our moving average framework for trend changes.

- We view the 200-day moving average (DMAVG) as a short-term trend change.

- We view the 55-week moving average (WMAVG) as an intermediate-term trend change.

- We view the 200-week moving average (WMAVG) as a cycle change.

Last Friday, the ratio closed below the 55-week moving average for the third consecutive week. Until these most recent weekly closes, the ratio had consistently closed above the 55-week moving average since December 2018, when the last interest rate hiking cycle ended.

To avoid a false start regarding making unnecessary asset allocation decisions, we seek to distinguish between a garden-variety index sell-off (i.e., 5-7% drawdown) and deep correction (i.e., >10% drawdown). After testing dozens of inputs for ~30 drawdowns more significant than 5% since the Global Financial Crisis, we find that the common denominator in our market correction framework is a close below the 55-week moving average for two consecutive weeks.

As you can see, there is a lot of real estate (i.e., >16%) between the 55-week moving average (i.e., an intermediate-term trend change) and the 200-week moving average (i.e., a cycle change).

Confirming an Intermediate-term Trend Change

Multi-year patterns are helpful for long-term price projections but not for timing. Therefore, it is prudent to establish a framework regarding a decisive and durable break of the ratio that would signify that the last eight months was a false COVID-related breakout.

To confirm the intermediate-term trend change, we are monitoring two indicators closely:

- The 20-week Average True Range (ATR) of the ratio is 0.034, just over 1.00%.

- The intraday low of the ratio on March 8, 2021, was 3.2170.

A weekly close below 3.2170 would be a new multi-month intraday low and more than two weekly ATR’s below that level. Therefore, we would view a weekly close of the ratio below 3.2170 as adequate evidence that the ratio is headed towards to the 200-week moving average, a cycle change.

Linkage Between NASDAQ-100 & 30-Year US Treasury Yields

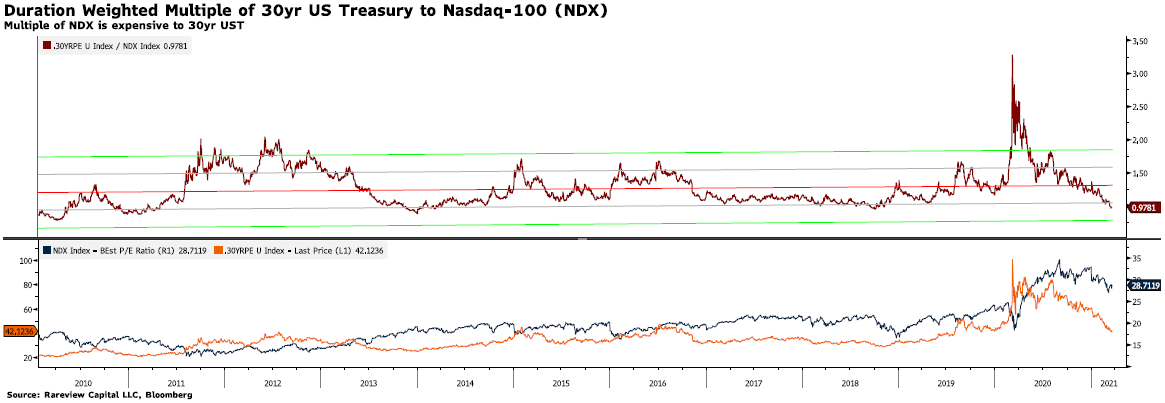

The following is specific to the absolute level of the NDX and the US Treasury market. On a duration-weighted basis, the NDX multiple is about the most expensive relative to 30-year US Treasury yields in the last decade.

The top section of the illustration below is a regression analysis of the duration-weighted multiple of the 30-year Treasury yield relative to the NDX. Note, the “duration” or “risk” of the NDX is roughly 1.5x the 30yr US Treasury yield. Therefore, the NDX is approximetly a 50-year asset.

The bottom section of the illustation below highlights that the NDX (blue line) multiple has not re-rated down despite the 30-year P/E (orange line) round tripping back to where it was in early 2020. If the 30-year Treasury yield were to rise another 25 to 50 bps in the short-term, it is likely that the NDX will have at least another 10% of downside. Otherwise, on a multiple basis, in the short-term, the price of the NDX will need to stay static or trend lower. Conversely, the 30-year yield could drop, but we think the outcome is less likely.

How Much Time Is Left in Interest Rates Rising?

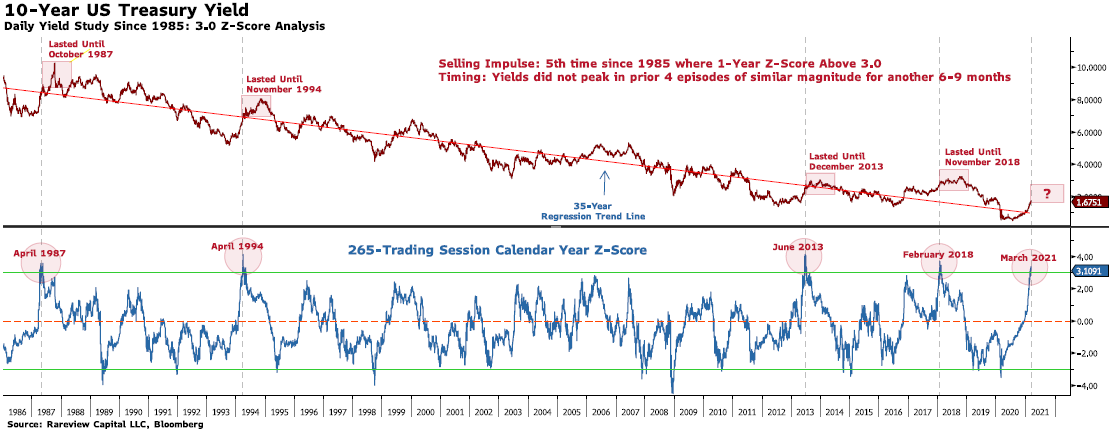

How does the current increase in interest rates compare to past episodes?

To answer this question, we screened past 10-year US Treasury yield moves for a one-year Z-score greater than 3.00. Currently, this is the fifth episode since 1985 where the 10-year yield moved more than 3-standard deviations in one year.

The rise in yields is approaching the 1987 surge, the 1994 bond massacre, the 2013 Taper Tantrum, and 2018’s Tax Cuts and Jobs Act.

In the prior four episodes of this magnitude, interest rates did not peak for another 6-9 months. Said differently, anxiety over higher interest rates should persist for the remainder of 2021.

Investment Implications

We believe the NASDAQ-100 Index will continue to underperform the S&P 500 Index if interest rates rise further. (Note: This is a relative value view, not a call that both indices will fall on an absolute basis.)

While the NDX/SPX ratio could fall materially, capturing the rotation at the sector and single security level may generate the most alpha. We have identified the potential winners and losers.

If you are interested in how we plan to adjust the allocations in our GROW strategies, please contact us. As a boutique firm, we can help you navigate these potential critical changes in the market by providing direct access to our investment professionals and library of tools. At Rareview Capital, our goal is to become a trusted resource and the first call for your questions. Please call us at 212-475-8664 or email us at info@rareviewcapital.com.

Recent Blog Posts

A Regime Change Occurred Last Week…Here Is How It Could Impact Your Portfolio

Concerned About Inflation? U.S. Government Bonds Are Not The Only Asset Class At Risk

More Yield, More Risk? You Might Be Surprised

Disclaimer

This material is for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any investment or any other security, including any investment with Rareview Capital LLC (“RVC”) or any of its affiliates or any other related investment advisory services. This material is not designed to cover every aspect of the relevant markets and is not intended to be used as a general guide to investing or as a source of any specific investment recommendation. This material does not constitute legal, tax, or investment advice, nor is it a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. In preparing this material, RVC has relied upon data supplied by third parties. RVC does not undertake any obligation to update the information contained herein in light of later circumstances or events. RVC does not represent the information herein is accurate, true or complete, makes no warranty, express or implied, regarding the information herein, and shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use. This material is subject to a more complete description and does not contain all of the information necessary to make any investment decision, including, but not limited to, the risks, fees and investment strategies of an investment. All investments carry a certain degree of risk, including the possible loss of principal. There is no assurance that an investment will provide positive performance over any period of time. There are specific risks that apply to investment strategies. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. RVC actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time. Closed-end funds frequently trade at a discount to their net asset value. These risks should be reviewed carefully before taking any investment action. Since no one investment style or manager is suitable for all types of investors, this site is provided for informational purposes only. The statements contained herein are the opinions of RVC. This site contains no investment advice or recommendations. Individual investor results will vary. Rareview Capital LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Past performance is no guarantee of future results.