by Neil Azous, Chief Investment Officer

The breakeven inflation rate is the difference between nominal yields and real yields. In early January, the entire U.S. Treasury breakeven inflation curve crossed above 2.0%. This has occurred less than 1% of the time in the past decade.

This event’s ramifications stretch beyond U.S. government bonds and now explicitly include corporate bond risk.

Why should you care about inflation risk on investment-grade credit? Because that sector makes up 12% of the industry’s dominant portfolio.

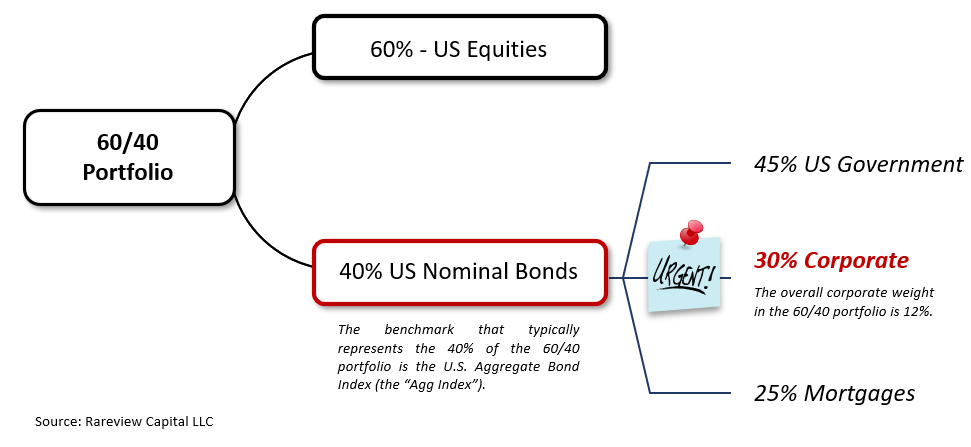

The traditional 60/40 portfolio is a “passive” mix of 60% U.S. equities and 40% U.S. nominal bonds. The benchmark that typically represents 40% of the 60/40 portfolio is the U.S. Aggregate Bond Index (the “Agg Index”). Using round numbers, the Agg Index’s weightings are 45% government, 30% corporate, and 25% mortgages.

By now, the low reward-to-risk setup of holding government securities is a consensus view. There is little room for yields to fall unless the Federal Reserve considers negative interest rates and no limit on how much they can rise. Add in the potential for a rise in inflation, and it is easier to understand why U.S. government securities could have a significant negative total return on both nominal and real interest rate bases.

But what about the much-less talked about 30% weighting of corporate bonds in the Agg Index?

Historically, investment-grade (I.G.) corporate bonds have provided a cushion for an unexpected inflation shock as spreads would tighten to offset higher interest rates. However, this is no longer the case because of tighter-than-normal credit spreads. Moreover, because of the low U.S. Treasury yields, the all-in yield of an I.G. bond portfolio offers much less offset than usual when interest rates rise. Finally, when inflation expectations are factored in, I.G. corporate bonds now have a negative real yield for the first time in history.

This inflection point arrives when duration risk is the highest in 20 years, and I.G. corporate credit spreads are near their all-time tight levels. This profile means that I.G. corporate bond returns are now very susceptible to even the slightest unexpected uptick in inflation.

Secondly, it is essential to understand this asset class’s recent evolution, which sometimes is overlooked given its lessor weighting to government securities in the benchmark.

Hopefully, by understanding this evolution vis a vis government bonds, the negative asymmetric return profile will be more readily apparent. This time, you can asset allocate your portfolio proactively.

When the Federal Reserve (the “Fed”) lowered U.S. interest rates to the Effective Lower Bound (ELB) in response to the pandemic, I.G. corporate bonds replaced U.S. Treasuries as the ballast in the 60/40 portfolio.

Simply put, the Fed’s reaction function changed. Alongside buying U.S. Treasuries and mortgages as part of its Quantitative Easing (“Q.E.”) program, the Fed began purchasing risky assets for the first time, including investment-grade credit. This new policy dynamic was announced on March 23, 2021. Not surprisingly, in retrospect, this marked the pandemic low for the S&P 500.

Finally, because of negative interest rates, it has been widely discussed that investors are paying foreign governments to lend them money. Over 40% of the world’s government bond markets have negative-yielding debt.

Now, this same phenomenon has extended to U.S. corporations. More than 25% of outstanding I.G. corporate bond issues are currently priced with a real yield below -0.50%. Said differently, one-fourth of IG-rated corporates are expected to be paid, on an inflation-adjusted basis, to borrow money today!

What Do You Do Now?

Adapting to rapid changes in the investment landscape has put dynamic asset allocation at the forefront of portfolio construction. Proof? It took 40 years for U.S. Treasuries to lose the accolade of “shock absorber.” I.G. corporate bonds only lasted 9-months as the replacement ballast in the 60/40 portfolio.

As the economy returns to full capacity, the risk of inflation increases. Thus, we believe investors must change their asset allocation to account for real interest rates instead of nominal outcomes.

U.S. Government and I.G. corporates should have minimal weight in a core fixed income strategy. Instead, investors should seek out active bond managers that combine the traditional benefits of a fixed income strategy with the advantages of non-traditional products.

We believe these managers have a greater chance of weathering potential inflation and reducing the erosion of purchasing power relative to off-the-shelf products.

At Rareview Capital, we are distinctly set up to help you.

As a boutique firm, we can support your business by providing direct access to our investment professionals and library of tools. We would be pleased to schedule an analysis of your income strategies to help you determine if you are taking the appropriate level of risk relative to the yield you are receiving. At Rareview Capital, our goal is to become a trusted resource and the first call for your questions. Please call us at 212-475-8664 or email us at info@rareviewcapital.com.

Disclaimer

This material is for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any investment or any other security, including any investment with Rareview Capital LLC (“RVC”) or any of its affiliates or any other related investment advisory services. This material is not designed to cover every aspect of the relevant markets and is not intended to be used as a general guide to investing or as a source of any specific investment recommendation. This material does not constitute legal, tax, or investment advice, nor is it a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. In preparing this material, RVC has relied upon data supplied by third parties. RVC does not undertake any obligation to update the information contained herein in light of later circumstances or events. RVC does not represent the information herein is accurate, true or complete, makes no warranty, express or implied, regarding the information herein, and shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use. This material is subject to a more complete description and does not contain all of the information necessary to make any investment decision, including, but not limited to, the risks, fees and investment strategies of an investment. All investments carry a certain degree of risk, including the possible loss of principal. There is no assurance that an investment will provide positive performance over any period of time. There are specific risks that apply to investment strategies. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. RVC actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time. Closed-end funds frequently trade at a discount to their net asset value. These risks should be reviewed carefully before taking any investment action. Since no one investment style or manager is suitable for all types of investors, this site is provided for informational purposes only. The statements contained herein are the opinions of RVC. This site contains no investment advice or recommendations. Individual investor results will vary. Rareview Capital LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Past performance is no guarantee of future results.