A Regime Change Occurred Last Week…Here Is How It Could Impact Your Portfolio

by Neil Azous, Chief Investment Officer

- The Next Sight Beyond Sight®

- Three Critical Signals

- Regime Shift

- Impact on Asset Classes: U.S. Equities, Gold, U.S. Dollar, Emerging Markets, TIPS

- A Final Warning

At Rareview Capital, we seek to bring a ‘rare view’ to investment challenges. We place value on being able to see across asset classes, discover new opportunities, identify hidden risks, and spot impending danger. We call this perspective Sight Beyond Sight®.

In our latest investment commentary – CONCERNED ABOUT INFLATION? U.S. GOVERNMENT BONDS ARE NOT THE ONLY ASSET CLASS AT RISK – we argued that investment-grade credit should have minimal weight in a portfolio. We were concerned because credit spreads were very tight, and even the slightest hint of inflation would lead to higher interest rates. So far, our Sight Beyond Sight® is proving correct. This year, as measured by the primary benchmark, investment-grade credit is -3.40%. For an asset with an average annual drawdown of 4.71%, this is a meaningful negative performance in a short period.

The Next Sight Beyond Sight®

Markets are a forward discounting mechanism, typically pricing outcomes at least six months in advance. Therefore, with the vaccination a fait accompli, it is prudent to begin thinking about macro themes beyond the pandemic’s evolution.

With that in mind, we believe the Sight Beyond Sight® is that higher 10-year real U.S. interest rates pose the most impending danger to current portfolio construction.

How can we see that? Last week, investors received critical macro information from the bond market.

Three Critical Signals

The nominal interest rate is the difference between real yields and breakevens. The breakeven rate is the difference in yield between inflation-protected and nominal debt.

Below is the U.S. Government bond market performance since February 10, 2021 close-of-business broken down by real, breakeven, and nominal interest rates.

As you can see, real interest rates exploded and breakevens declined modestly.

Note, a one-standard-deviation move in 10-year real U.S. interest rates over six days is 10 basis points. Since February 10th, real yields rose from -1.07% to -0.82% or 2.5-standard-deviations. Technically, real yields broke out of their multi-month range and crossed above the 200-day moving average for the first time since January 2019.

At a minimum, there are two potential key takeaways:

- A floor in real interest rates has been solidified.

- Real yields are unlikely to decline further.

Next, while the degree of the absolute sell-off in real interest rates and the reversal in breakevens are proof-enough of regime change, at Rareview Capital, we seek an additional confirmation from hard-to-see places. One area that provides strong signaling power is yield curvature. For example, the nominal yield curve had a noticeable change in leadership regarding the recent steepening bias.

Until last week, the steepening was led by the yield curve’s 5/30-year slope, driven by inflation expectations in the long-end. Now, the 2/5-year slope is leading, powered by Federal Reserve expectations in the belly of the curve. Combining the two slopes into a 2/5/30-year butterfly best encapsulates the phase shift underway. Last Tuesday, the “butterfly” had its largest one-day move in yield since the 2016 U.S. Presidential Election.

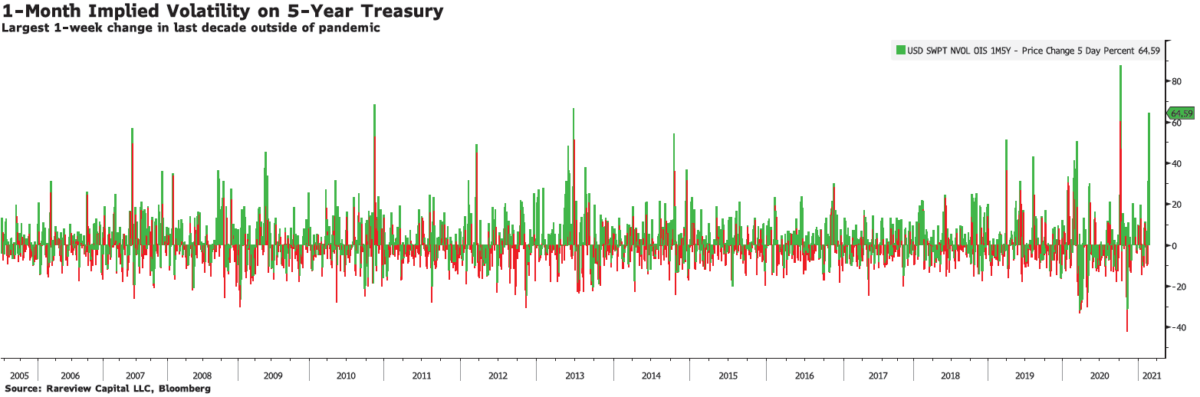

Finally, our long history in credit and equity derivatives allows us to look at volatility in multiple dimensions. We see that bond volatility flashed a critical signal that mirrors the messaging received from real rates and the nominal yield curve. For example, last week’s relative change of implied volatility of a one-month option on the 5-year U.S. Treasury rose by 3-standard deviations. In absolute terms, it was the largest move higher in a decade, outside of the pandemic, and close to the highs of the last 15 years.

Collectively, we believe the bond market signaled that the current economic scenario of growth and reflation optimism would soon lead to a step-change in the Federal Reserve outlook. That is, a tightening stance, away from pandemic-led easing. Note, this is the phase before an interest rate hiking cycle begins.

Regime Shift

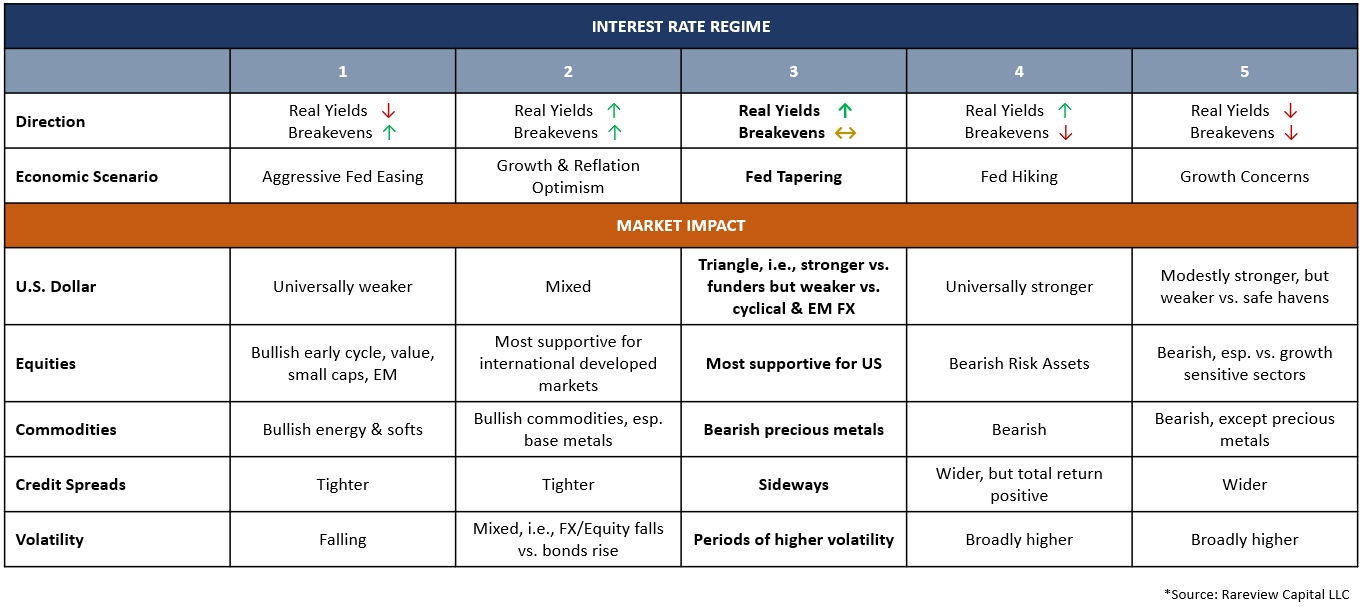

Below is a regime matrix for real yields and breakevens. Based on the three critical signals received last week, we believe the bond market shifted from Regime 2 to Regime 3.

As we advance, we expect a more gradual rise in real yields and breakevens to move sideways in response to robust economic data over the coming months. Note, the last time we were in Regime 3 in 2013, Federal Reserve messaging drove the regime change, which led to the “taper tantrum.” Recognizing this distinction is critical.

Higher real yields are typically associated with a stronger U.S. dollar and lower gold prices. They are usually a headwind for equities, especially if the upward move is fast and steep. However, we are not at the point where the U.S. dollar will be universally stronger, or that risky assets and commodities will broadly fall because of higher real interest rates. Why? Because that occurs during the transition from Regime 3 to Regime 4 when the Federal Reserve telegraphs a hiking cycle when they begin tapering asset purchases.

Impact on Asset Classes

Based on the transition from Regime 2 to 3 with the Federal Reserve caveat, below is our Sight Beyond Sight® for various asset classes.

US Equities: The S&P 500 typically falls 1.5-2.0% following a 2-standard deviation move higher in real yields in one month. That said, we are less worried about the stock market if:

- The speed and degree of the next real yield move is incremental.

- The absolute level of the real yield is still negative.

- Earnings growth remains strong.

Commodities: Gold is the commodity most inversely correlated to higher real yields. The yellow metal fell 2.80% last week. There was also a key bearish technical development. That is, a “Death Cross” formed where the 50-day fell below the 200-day moving average. The last five times that happened since 2010, gold fell ~13% on average. Above other assets, gold is the most apparent casualty currently and should continue to trade soft, especially as cryptocurrencies continue to take inflows away from it.

US Dollar: The US dollar has yet to universally strengthen, especially against cyclical or emerging market currency crosses because government bond yields in the rest of the world have been rising at a faster pace than US Treasuries in February. That will change when/if messaging leads to front-end rates repricing meaningfully as shorter-dated yields matter most for exchange rates. For now, investors are slowly rotating to other low-yielding funding currencies – the euro exchange rate (EUR), Japanese yen (JPY), and Swiss franc (CHF). This funding switch argues that if you are a US-based investor holding European or Japanese equities, it is prudent to move into the currency-hedged versions of those products. Three ETF examples include HEDJ, DXJ, and AXJ.

Emerging Markets: One asset class that should be singled-out for impending danger is emerging markets. Both equities and local currency debt are extremely sensitive to a stronger U.S. dollar and higher real interest rates. There is also growing fear that China is tightening policy after weathering the pandemic better than other G7 countries. Recently, a key reflation metric for the world – their fiscal impulse – turned down. A continuation in the “world’s factory” would signal that the manufacturing-over-services trade is complete. If you are overweight, the traffic light just turned to yellow for a downgrade to neutral from overweight.

Treasury Inflation-Protected Securities (TIPS): The industry’s dominant portfolio – the 60/40 stock-bond allocation – has undergone a structural change since last summer. For months, institutional investment managers, including us, have advocated replacing the 40% nominal bond allocation with inflation-linked bonds and commodities. As a result of that rotation, the current valuation of TIPS discounts the outcome of above-trend inflation. Said differently, TIPS are fully valued, and there is little room for error. The regime shift by the Federal Reserve has negative implications for TIPS securities. As real yields increasingly discount a tighter policy path from the Federal Reserve, the price of TIPS declines. Moreover, if the market continues to price a faster tightening path because of an increase in inflation, the expected offset to inflation pressures cannot be TIPS. Why? Because TIPS may become a detriment when accounting for the low absolute negative real yield.

A Final Warning

One final crucial risk warning is warranted. Regarding risk management, we are often asked what keeps us up at night? The answer is a twin-move of higher real interest rates and lower crude oil prices. Fundamentally, we are currently very constructive on the barrel – its high roll-yield is hard to ignore. However, on March 31st, OPEC+ is expected to curtail their production cuts. Also, the WTI oil strip is nearing levels that may entice US shale producers to focus on Free Cash Flow (FCF) instead of CAPEX discipline. We are watching this risk profile above all else because it typically leads to credit spread widening, and credit spreads are at/near all-time tight levels. Also, there is no hedge to this scenario except higher cash balances before it happens. If this scenario materializes, the ripple effect will be felt hard across risk assets.

As a boutique firm, we can help you navigate these potential critical changes in the market by providing direct access to our investment professionals and library of tools. At Rareview Capital, our goal is to become a trusted resource and the first call for your questions. Please call us at 212-475-8664 or email us at info@rareviewcapital.com.

Disclaimer

This material is for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any investment or any other security, including any investment with Rareview Capital LLC (“RVC”) or any of its affiliates or any other related investment advisory services. This material is not designed to cover every aspect of the relevant markets and is not intended to be used as a general guide to investing or as a source of any specific investment recommendation. This material does not constitute legal, tax, or investment advice, nor is it a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. In preparing this material, RVC has relied upon data supplied by third parties. RVC does not undertake any obligation to update the information contained herein in light of later circumstances or events. RVC does not represent the information herein is accurate, true or complete, makes no warranty, express or implied, regarding the information herein, and shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use. This material is subject to a more complete description and does not contain all of the information necessary to make any investment decision, including, but not limited to, the risks, fees and investment strategies of an investment. All investments carry a certain degree of risk, including the possible loss of principal. There is no assurance that an investment will provide positive performance over any period of time. There are specific risks that apply to investment strategies. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. RVC actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time. Closed-end funds frequently trade at a discount to their net asset value. These risks should be reviewed carefully before taking any investment action. Since no one investment style or manager is suitable for all types of investors, this site is provided for informational purposes only. The statements contained herein are the opinions of RVC. This site contains no investment advice or recommendations. Individual investor results will vary. Rareview Capital LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Past performance is no guarantee of future results.