STOCK MARKET CORRECTION FRAMEWORK

by Neil Azous, Chief Investment Officer

- INTRODUCTION

- TWO TYPES OF CORRECTIONS

- ALL CORRECTIONS

- TYPE 1 CORRECTION

- TYPE 2 CORRECTION

- CONCLUSION

INTRODUCTION

We utilize this framework as a guidepost for a stock market correction’s potential depth and length. This is not a prediction or bold call for a bear market. Remaining open-minded about the downside possibilities helps us with risk management and when to transition away from defensive positioning.

TWO TYPES OF CORRECTIONS

We integrate moving averages into the framework. We view:

- The 200-day moving average (DMAVG) as a short-term trend change;

- The 55-week moving average (WMAVG) as a medium-term trend change;

- The 200-week moving average (WMAVG) as a cycle change.

There are two types of corrections:

- Type 1: A 7-13% drawdown where the SPX trades below the 200-DMAVG for less than two weeks.

- Type 2: A 13-21% drawdown where the SPX trades below the 200-DMAVG for 30-90 days.

The common denominator for the transition to Type 2 from Type 1 is the 55-week MAVG. Specifically, the S&P 500 must close below the 55-WMAVG for two consecutive weeks.

Last Friday, April 22nd, the stock market transitioned to Type 2 – a more profound and prolonged correction.

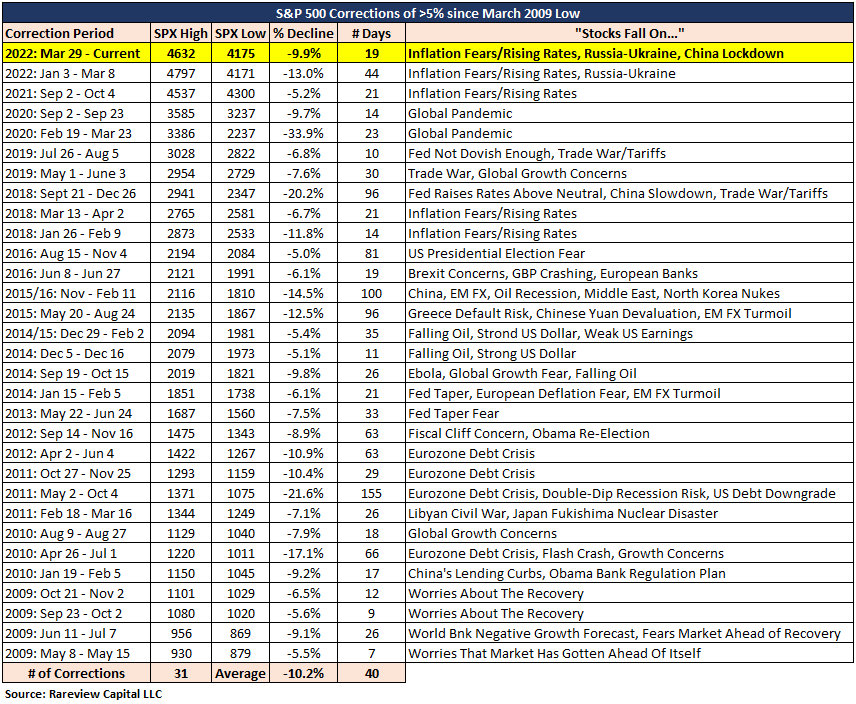

ALL CORRECTIONS

Including the current one, there have been 31 corrections deeper than 5% since the March 2009 global financial crisis low.

The table below shows you the correction period, the SPX Index high-low, percentage decline, the number of calendar days the decline lasted, and why stocks fell.

The average drawdown is -10.2% and lasts 40 days on average.

That said, we believe the signaling power from this broad sample set is low quality. In the next sections, we provide a framework that separates the correction into two types – one that is garden variety and one that could have a detrimental impact on a portfolio.

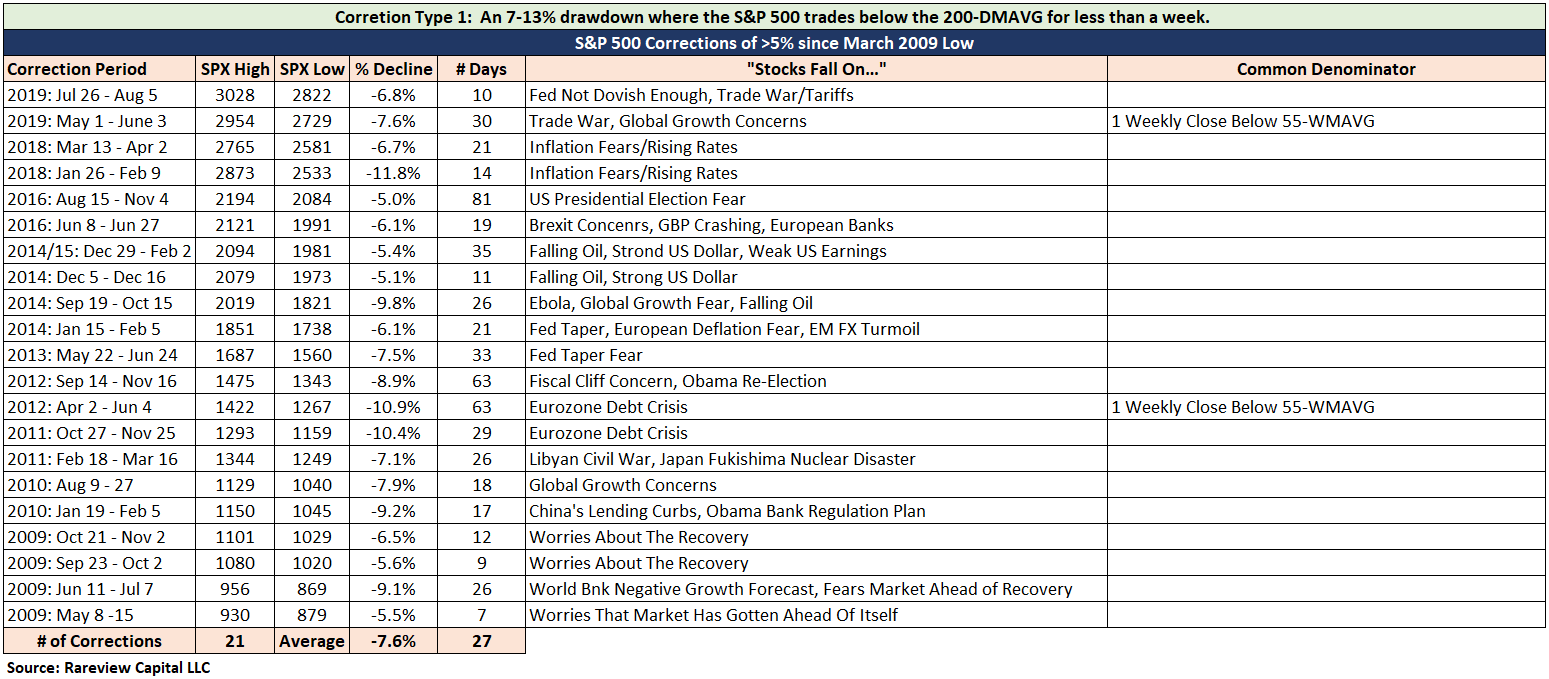

TYPE 1 CORRECTION

Of the 31 corrections, 21 of them fall into Type 1.

We define a Type 1 correction as a 7% to 13% drawdown where the S&P 500 typically trades below the 200-DMAVG for less than a week.

The table below shows the average drawdown is -7.6% and lasts 27 days on average.

Type 1 corrections have nothing in common. It is usually confined to short-term events, including a US government shutdown, country rating downgrades, growth scare (different than a contraction), or a significant and fast move in a critical asset, such as the US dollar or crude oil.

Common Denominator: None.

TYPE 2 CORRECTION

Of the 31 corrections, 8 of them fall into Type 2.

We define a Type 2 correction as a 13% to 21% drawdown where the S&P 500 typically trades below the 200-DMAVG for 30-90 days.

The table below shows the average drawdown is -17.8% and lasts 75 days on average.

Unlike Type 1, Type 2 corrections have one thing in common: the event is a “heart attack.” Historically, it results from a Federal Reserve hiking cycle, Chinese yuan devaluation, Eurozone crisis, or the start of a growth contraction that leads to a recession.

Common Denominator: The SPX recorded two consecutive “weekly” closes below the 55-WMAVG.

CONCLUSION

If the stock market falls below the 55-WMAVG moving average for two weeks, the sell-off tends to end much lower, near the 200-WAMVG, and is much more protracted in time.

Simultaneously, other asset classes fall. This is especially true if credit and crude oil are involved. Why? Because there is no hedge to higher real interest rates, wider credit spreads, and the barrel falling at the same time. This causes a VaR shock to models as volatility is too hard to control. The only remedy is to reduce risk.

Secondly, equity derivative trading desks and quantitative equity research groups add little value during Type 2 corrections outside of providing recovery statistics. Their 15 minutes of fame typically occurs in the first 3-7% drawdown during a Type 1 correction. In Type 2 corrections, the driving force is a global margin call on retail investors. Their fund outflows are significantly larger than when alternative strategies reduce risk.

Thirdly, when a correction is transitioning to Type 2 from Type 1, it is a mistake to rely on indicators in isolation: put/call ratio, AAII sentiment, VIX curve inversion, technicals, positioning, etc. Why? Because just prior to when the 200-WMAVG is confirmed, all of these indicators concurrently test “all-time” or make ”all-time” record readings. If you rely on one indicator or try to back-fit a reason to buy weakness by fusing several and are wrong, the 200-WMAVG is another -17% down (i.e., SPX 3462).

———-

If you are interested in learning about our “recovery framework” we use to become less defensive, including how to potentially navigate the various types of recoveries, please contact us.

Rareview Capital LLC is a registered investment adviser and ETF sponsor. We build goals-based investment management strategies that can be accessed through ETFs, sub-advisory/dual contract, model portfolios, or by opening an account directly with us.

If you have any questions or would like to hear more about our ETFs, please call us at 212-475-8664, or email us at info@rareviewcapital.com.

DISCLAIMER

This material is for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any investment or any other security, including any investment with Rareview Capital LLC (“RVC”) or any of its affiliates or any other related investment advisory services. This material is not designed to cover every aspect of the relevant markets and is not intended to be used as a general guide to investing or as a source of any specific investment recommendation. This material does not constitute legal, tax, or investment advice, nor is it a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. In preparing this material, RVC has relied upon data supplied by third parties. RVC does not undertake any obligation to update the information contained herein in light of later circumstances or events. RVC does not represent the information herein is accurate, true or complete, makes no warranty, express or implied, regarding the information herein, and shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use. This material is subject to a more complete description and does not contain all of the information necessary to make any investment decision, including, but not limited to, the risks, fees and investment strategies of an investment. All investments carry a certain degree of risk, including the possible loss of principal. There is no assurance that an investment will provide positive performance over any period of time. There are specific risks that apply to investment strategies. Since no one investment style or manager is suitable for all types of investors, this site is provided for informational purposes only. The statements contained herein are the opinions of RVC. This site contains no investment advice or recommendations. Individual investor results will vary. Rareview Capital LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Past performance is no guarantee of future results.