DEMYSTIFYING THE PRICING OF INTEREST RATE CUTS

by Michael Sedacca, Portfolio Manager

- INTRODUCTION

- BACKGROUND

- MISCONCEPTION ABOUT CUTS

- WEIGHTING PROBABILITY RISKS

- CONCLUSION

INTRODUCTION

Many are confused about why the US fixed income market is pricing interest rate cuts in 2023, with inflation at a high level and the unemployment rate at a low level. The following commentary seeks to dispel the misconceptions surrounding why the pricing for these interest rate cuts exists.

Note that this commentary is not about inflation or employment. It is not a forecast. It is about probabilistic outcomes and historical precedent driving market pricing, regardless of the economic data or Federal Reserve messaging.

BACKGROUND

Neutral Rate: At its July meeting, the Federal Reserve raised interest rates to a 2.5% target band. In Rareview Capital’s White Paper, we identified the neutral Fed funds rate at 2.14%. The Fed reached and moderately surpassed the neutral rate at the July meeting. This is unequivocal.

Time to Cut After Hikes End: On average, since 1970, the Fed has cut interest rates 6.5 months following the last interest rate hike. The quickest was 1.4 months. The longest was 14.7 months, the only time out of eight cycles that took longer than 7.5 months. Finally, during the oft-discussed 1980 cycle, the Fed cut interest rates in the same week as an interest rate hike more than once.

Cuts After Hikes: Following interest rate hikes of at least 3%, the historical probability that the Fed funds rate will be lower in the next 12 months is 91% (i.e., 8 out of 9 times). Only one cycle in the post-WWII era saw interest rate cuts less than the total amount of hikes – in 1995. Coincidentally, this was the lowest amount that the Fed raised interest rates beyond the neutral rate, which necessitated fewer interest rate cuts to offset the overtightening. More often than not, the amount of interest rate cuts exceeded the total amount of interest rate hikes.

Speed of Cuts: On average, the Fed has cut interest rates at 2.4 times the speed it raised. Said differently, if a Fed tightening cycle lasted two years, they would likely cut interest rates by the total amount of hikes in 10 months once those cuts began.

MISCONCEPTION ABOUT CUTS

Most market participants look at the pricing of interest rate cuts in the absolute and see these as being “wrong” or “right.” They are unaware that interest rate pricing is primarily based on the probability of a wide variety of outcomes occurring, especially regarding short-term interest rates.

For example, between now and the end of 2023, there will be 11 Federal Reserve meetings and the non-negligible possibility of inter-meeting policy shifts. At each of those meetings, the Fed could raise or lower interest rates by more than 25 basis points. Each outcome is assigned a probability. Theoretically, there are hundreds of potential outcomes when all 11 meetings are factored in, including a 25 basis points hike, a 50 basis points hike, a 25 basis point cut, a 50 basis point cut, etc.

WEIGHTING PROBABILITY RISKS

The current Fed funds target rate is 2.5%. The Fed will likely raise short-term interest rates by at least 25 basis points at the September and November meetings. This will bring the total amount of interest rate hikes to at least 3%. The length of the cycle will be seven months old at that point. The historical precedent is that interest rates are cut 91% of the time in the next 12 months after a 3% increase in the Fed funds target rate.

The expected peak Fed funds rate is 3.75%-4% and will drop to 3.25%-3.5% in 2023.

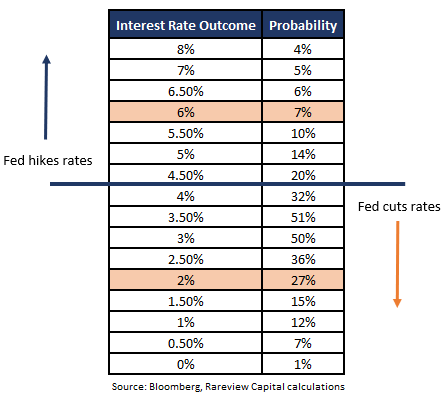

Therefore, if the Fed funds rate is discounted in the market at ~4%, which would you believe is the higher potential risk, a cut to 2% or further hikes to 6%? The US fixed income market has answered that question. It is placing a 27% probability of a cut to 2% relative to a 7% probability of further hikes to 6%. That equates to a 4 to 1 chance of the Fed funds rate ending 2023 at 2%.

The table to the right shows the probability of an interest rate outcome being realized according to the market.

CONCLUSION

We believe anyone’s view on portfolio construction beyond these facts is subjective and is not supported by the overwhelming evidence for central bank decision-making.

From a probabilistic outcome perspective and based on historical precedent, it is, therefore, logical to expect:

- The Fed’s future interest rate cuts could be swift, mainly because the current interest rate hiking cycle can be measured in months rather than years.

- If the last interest rate hike takes place in late 2022, the odds of an interest rate cut in 2023 are nearly certain.

- The precedent of the Fed cutting interest rates back to zero in the next two years is very high. Ironically, per the table above, the market is only pricing in a 1% probability of that outcome.

This explains why the interest rate market is priced for the relatively higher risk of substantial interest rate cuts over the next two years.

———-

If you are interested in learning about our proprietary interest rate investment process and how we navigate the various Federal Reserve regimes, please contact us.

Rareview Capital LLC is a registered investment adviser and ETF sponsor. We build goals-based investment management strategies that can be accessed through ETFs, sub-advisory/dual contract, model portfolios, or by opening an account directly with us.

If you have any questions or would like to hear more about our ETFs, please call us at 212-475-8664, or email us at info@rareviewcapital.com.

DISCLAIMER

This material is for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any investment or any other security, including any investment with Rareview Capital LLC (“RVC”) or any of its affiliates or any other related investment advisory services. This material is not designed to cover every aspect of the relevant markets and is not intended to be used as a general guide to investing or as a source of any specific investment recommendation. This material does not constitute legal, tax, or investment advice, nor is it a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. In preparing this material, RVC has relied upon data supplied by third parties. RVC does not undertake any obligation to update the information contained herein in light of later circumstances or events. RVC does not represent the information herein is accurate, true or complete, makes no warranty, express or implied, regarding the information herein, and shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use. This material is subject to a more complete description and does not contain all of the information necessary to make any investment decision, including, but not limited to, the risks, fees and investment strategies of an investment. All investments carry a certain degree of risk, including the possible loss of principal. There is no assurance that an investment will provide positive performance over any period of time. There are specific risks that apply to investment strategies. Since no one investment style or manager is suitable for all types of investors, this site is provided for informational purposes only. The statements contained herein are the opinions of RVC. This site contains no investment advice or recommendations. Individual investor results will vary. Rareview Capital LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Past performance is no guarantee of future results.