REGIME SHIFT…TIME TO FIGHT THE FED…ASSET ALLOCATION UPDATE

by

Neil Azous, Chief Investment Officer

Michael Sedacca, Portfolio Manager

- FEDERAL RESERVE HIKING CYCLE

- CERTAINTY IS THE INABILITY TO IMAGINE THE ALTERNATIVE

- FUNDAMENTAL ANALYSIS

- REGIME SHIFT

- TIME TO FIGHT THE FED

- EXTEND DURATION

- 60/40 REBORN

INTRODUCTION

A key distinction between fixed income and other asset classes is that the yield curve and vast array of available instruments allow you to recreate scenario analysis precisely.

We have assembled the following pieces of the fixed income puzzle.

PROBABILISTIC OUTCOMES > FUNDAMENTAL ANALYSIS > REGIME MAPPING > 60/40

The interest rate hiking cycle is no longer a mystery. Therefore, we are ready to “fight the Fed” and make significant fixed income portfolio construction changes.

FEDERAL RESERVE HIKING CYCLE

The current Fed funds rate is 2.50%. The table below shows the key fixed income metrics relative to the current Fed funds rate:

| METRIC | RATE | NOTES |

| Neutral Rate – Rareview Capital | 2.14% | Currently above our neutral rate, see White Paper |

| Neutral Rate – Federal Reserve | 2.375% | Slightly above the Fed’s neutral rate |

| Federal Reserve December 2022 Target | 3.40% | The current market terminal rate is 3.85% in November-December 2022 period |

| Federal Reserve December 2023 Target | 3.80% | The market is priced above the terminal rate one year early |

The table below shows what is presently priced in the US fixed income futures market:

| FOMC MEETING | PATH | EXPECTED FED FUNDS RATE |

| September 21, 2022 | “Maybe” a 75 bps hike | 3.25% |

| November 2, 2022 | “Certain” of a 50 bps hike | 3.75% |

| December 14, 2022 | “Certain” of a 25 bps hike | 4.00% |

| February 2, 2023 | “Maybe” a 25 bps hike | 4.25% |

| March 22, 2023 | Pause | 4.25% |

| May 3, 2023 | Interest rate cut | 4.00% |

| Beyond | 50-100 bps of interest rate cuts until December 2025 | 3.50%-3.00% |

Between March to July 2022, the Fed asymmetrically hiked interest rates from 0.25% to 2.50%. In Fed speak, this is known as “early cycle.”

Using sports metaphors, “half-time” or the “seventh inning stretch” is when the Fed raises interest rates above the neutral rate, which occurred at the July 27th FOMC meeting.

Definition: The “neutral rate” is the prevailing rate at which the economy runs at its potential – without overheating or excessively cooling down.

Again, using Fed speak, the period above the neutral rate is called the “late cycle” because it is considered a restrictive policy.

In our White Paper, A ‘Rare View’ That Pinpoints The Neutral Rate Before A Hiking Cycle Begins, we calculated this cycle’s neutral rate at 2.14% (vs. Fed’s 2.375%). Furthermore, we analyze the average amount that the Fed funds rate exceeds Rareview Capital’s determination of the neutral rate in two dimensions:

1. Ex-post the Cycle: The average is 0.82%. The lowest is 0.60%. The highest is 1.33%.

| NEUTRAL RATE | EXCEEDS | ABOVE NEUTRAL | NOTES |

| 2.14% | Lowest = 0.60% | 2.74% | Fed funds will be at a minimum of 3.00% at the September FOMC meeting |

| 2.14% | Average = 0.82% | 2.96% | Fed funds will “likely” be at 3.25% at the September FOMC meeting |

| 2.14% | Highest = 1.33% | 3.47% | Fed 2023 target 3.80%, Current Terminal Rate Pricing = 3.85% |

2. During the Cycle: The average is 1.21%. The lowest is 0.75%. The highest is 1.72%

| NEUTRAL RATE | EXCEEDS | ABOVE NEUTRAL | NOTES |

| 2.14% | Lowest = 0.75% | 2.90% | Fed funds will be at a minimum of 3.00% at the September FOMC meeting |

| 2.14% | Average = 1.21% | 3.35% | Fed funds will “likely” be at 3.25% at the September FOMC meeting |

| 2.14% | Highest = 1.72% | 3.86% | Fed 2023 target = 3.80% vs. Current Terminal Rate Pricing = 3.85% |

Of the two dimensions analyzed, we focus on the pricing “during the cycle” because it is more extreme than the data on an “ex-post” basis. Put another way, if we are wrong, we will lose from a starting point that has 1-2 additional 0.25% interest rate hikes priced-in. Therefore, the following data points only apply to the “during the cycle” analysis and exclude the “ex-post” data.

Following an expected 0.75% interest rate hike at the September 21st FOMC meeting, the Fed funds rate will be 1.11% above the neutral rate (i.e., 3.25% Fed Funds minus 2.14% neutral rate = 1.11% above).

Note that the Fed funds rate will be modestly higher than the average overshoot above the neutral rate (i.e., 3.25% vs. 3.35). However, raising (or cutting) interest rates is considered a “blunt” tool. Therefore, 3.25% is close enough to the average overshoot of “neutral.”

Also, 0.75% of further interest rate hikes are priced in the market between November and December. If this pricing is realized, the Fed funds rate will be above the highest overshoot of “neutral” (i.e., 4.00% vs. 3.86%).

The critical point is that whatever investment decision you make will be either on par with the average overshoot currently or likely above the highest overshoot by December.

Put another way, if you buy a bond today, you will only lose money if this Federal Reserve hiking cycle surpasses the highest overshoot above the neutral rate by a substantial margin. Even in this instance, a loss is incremental because further rate hikes would likely be spread out, and the high coupon you receive along the way would act as a cushion.

CERTAINTY IS THE INABILITY TO IMAGINE THE ALTERNATIVE

When navigating the contours of a Federal Reserve interest rate cycle, the professional implementation of a fixed income portfolio should mainly be based on probabilistic outcomes.

We believe anyone’s view on portfolio construction beyond this discipline is subjective and is not supported by the overwhelming evidence for central bank decision-making.

In our recent investment commentary – Demystifying The Pricing Of Interest Rate Cuts – we demonstrate why probabilistic outcomes and historical precedent drive market pricing, regardless of the economic data or Federal Reserve messaging.

We would rather have the information below than hold an opinion about the current employment trend or what a member of the Fed said at a recent conference. Why? Because probabilistic outcomes are generated from these variables, not subjectivity. This allows us to construct a portfolio based on the highest expected outcome.

- The Neutral Rate (Fed = 2.375%, Rareview Capital = 2.14%)

- The average amount the Fed hikes interest rates above the neutral rate (i.e., by 0.1.21%)

- The extreme amount the Fed hikes interest rates above the neutral rate (i.e., by 1.72%)

- The last interest rate hike (i.e., expected in December 2022)

- The quickest (1.4 months), average (6.5 months), and longest (14.7 months) time the Fed cuts interest rates after the last hike

- The speed at which the Fed cuts interest rates (i.e., 2.4 times the speed it raised interest rates)

FUNDAMENTAL ANALYSIS

To further validate our asset allocation decision-making, we marry the probabilistic outcome discipline with fundamental analysis.

We monitor dozens of market-based measures in our proprietary investment process to determine when the interest rate hiking cycle transitions to a new regime.

We have narrowed these variables to six measures that best encapsulate a regime shift.

Note: We do not disclose the six variables as they are closely guarded.

We weight these six variables based on forward 3-month, 6-month, and 12-month excess returns of the Bloomberg Barclays US Treasury Index. Note that this benchmark index currently has a 7.86-year time to maturity or has similar duration characteristics as an intermediate bond.

| TIME FRAME | TOTAL RETURN | EXCESS RETURN |

| 3-months | 1.84% | 0.69% |

| 6-months | 6.81% | 4.51% |

| 12-months | 13.53% | 8.93% |

Definition: Total Return is price return plus coupons received. Excess Return is the return of a bond over its coupon over a period. That is, the amount the yield fell or rose.

Recently, all six measures crossed our threshold to constitute a regime shift.

In past cycles, when these six triggers are all met, the Fed has never raised interest rates beyond the next 1-2 meetings. Therefore, current market pricing suggests that the last rate hike will occur at the November or December meetings.

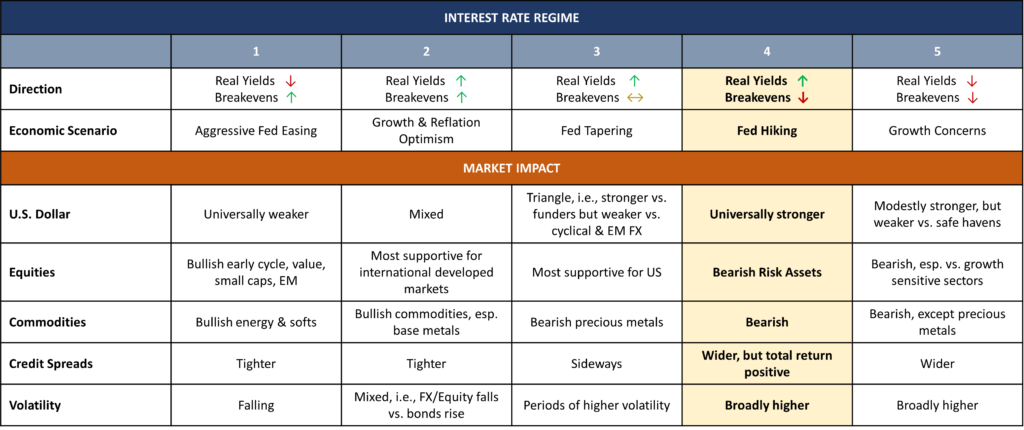

REGIME SHIFT

To the right is our regime matrix for real yields and breakevens.

Definition: A real interest rate is the difference between a nominal interest rate and the rate of inflation. The breakeven inflation rate is a market-based measure of expected inflation. It is the difference between the yield of a nominal bond and an inflation-linked bond of the same maturity.

Based on the critical signals received recently in our proprietary framework, we believe the bond market is undeniably in Regime 4. That is, real yields are rising, and breakevens are falling.

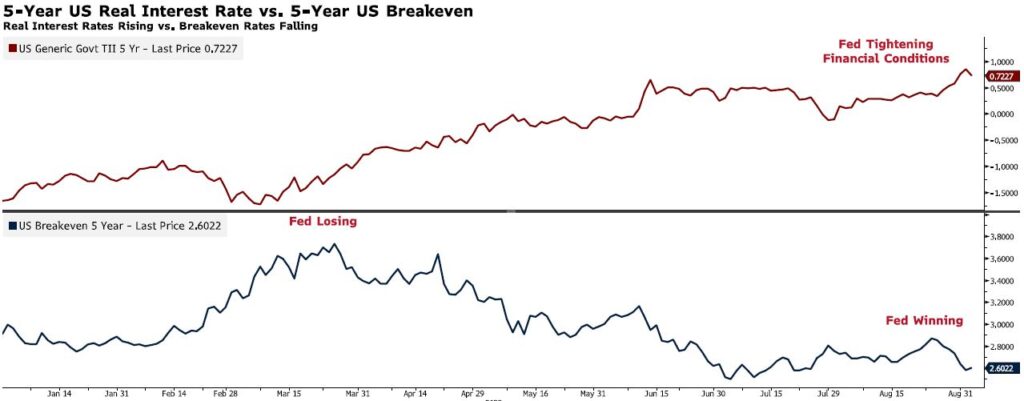

Last week, the 5-year US real interest rate closed at 0.72%. Note that the move higher in real yields last Friday surpassed the cycle high recorded in June (i.e., 0.70%). Notably, this occurred on a “monthly” closing basis, which we believe has more validity for a thematic portfolio than a “weekly” or “daily” close.

Concurrently, the 5-year US breakeven interest rate closed at 2.60%, below the January-February range. Inflation expectations are now near their lowest point of the interest rate hiking cycle.

Collectively, these charts show the Fed is tightening financial conditions and winning the battle against inflation expectations. That happens when you raise interest from 0.25% to 4.25% in six months. Note that the Fed has raised rates to 2.50% in the spot market and 4.25% in the futures market.

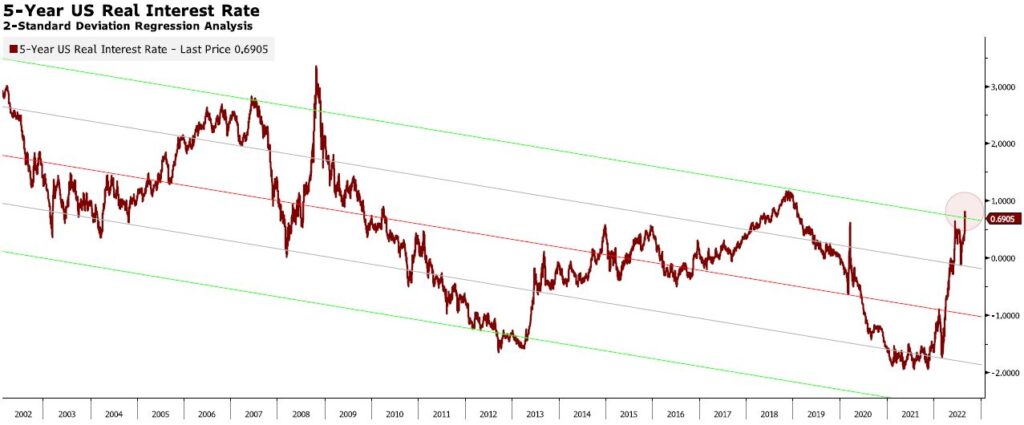

To further demonstrate the “blunt” force of the Fed’s hand, below is a daily chart of the 2-standard deviation regression of the 5-year US nominal interest rate minus the 5-year US breakeven interest rate dating back to 2002. As you can see, US real interest rates are now the driving force of financial conditions to the degree that they are trading outside the 2-standard deviation band.

We believe that 5-year US real interest rates surpassing the year’s highs are a milestone. Why? Because positive real interest rates are central to a Fed strategy of tightening financial conditions (i.e., stronger US dollar, wider credit spreads, weaker equities, etc.). It means their policy is moving from moderately restrictive to aggressively restrictive.

Historically, a 5-year US real interest rate range between 1.00% to 1.50% is recessionary. The 5-year US real interest rate at 0.72% is still below the 1.00%-1.50% range and may be challenging to attain if the input is solely a rise in nominal interest rates. However, 0.25%-0.75% higher is not that far away if the inputs are higher nominal rates and lower inflation expectations by December, which the Fed is trying to engineer with another 1.25% to 1.50% Fed fund hikes.

TIME TO FIGHT THE FED

Extend Duration

When the Fed reaches the point of “breaking the market” in Regime 4, counterintuitively, the most positive response is in long-duration assets. Why? Because once this stage is reached, the subsequent policy response is to cut interest rates within 6.5 months on average.

Therefore, as we reach the average point above the neutral rate this month or surpass the extreme overshoot of the neutral rate by December, the significant fixed income portfolio construction change is to extend the duration.

We have started that process in the products we manage.

60/40 Reborn

As a result of the shift in the inflation outlook, the increase in the stock-bond correlation this year far exceeded what most anticipated. This occurred despite historical precedent. Still, investors with a balanced portfolio experienced a historical drawdown. In response, the sentiment is that the 60/40 stock-bond portfolio is dead or badly impaired.

We find this view pedestrian. Below, we present a more nuanced outlook of what to expect from a “balanced” portfolio as we advance.

In our framework, stock-bond correlation depends on the type of shock to the economy.

For example, the environment that delivers the effective hedging properties of Treasury securities tends to prevail when the most active shock to the economy is related to changes in the strength of economic growth or investors’ risk appetite. This is what occurs “late” in a Fed hiking cycle, such as now.

Conversely, when a shock is driven by unstable inflation expectations or perceived shifts in the Federal Reserve’s reaction function, stock-bond correlation increases, impairing the Treasuries’ hedging properties. This is what occurs “early” in a Fed hiking cycle, such as the period of March-July.

Below is a summary of this framework.

| SHIFT IN | INFLATION EXPECTATIONS | MONETARY POLICY REACTION FUNCTION | EXPECTED GROWTH | INVESTOR RISK APPETITE |

| Stock-Bond Correlation | Positive | Positive | Negative | Negative |

Overall, the stock-bond correlation may remain near zero or even be positive while inflation concerns persist or remain elevated. However, with shifts in expected growth and investor appetite being the drivers of stock-bond correlation in Regimes 4, 5, and 1, the most likely outcome is that the hedging-friendly correlation properties of US Treasuries will be “reborn” soon. This is truer now that the starting point for buying a bond is a ~4% terminal interest rate.

If you are interested in learning about our proprietary interest rate investment process and how we navigate the various Federal Reserve regimes, please contact us.

Rareview Capital LLC is a registered investment adviser and ETF sponsor. We build goals-based investment management strategies that can be accessed through ETFs, sub-advisory/dual contract, model portfolios, or by opening an account directly with us.

If you have any questions or would like to hear more about our ETFs, please call us at 212-475-8664, or email us at info@rareviewcapital.com.

DISCLAIMER

This material is for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any investment or any other security, including any investment with Rareview Capital LLC (“RVC”) or any of its affiliates or any other related investment advisory services. This material is not designed to cover every aspect of the relevant markets and is not intended to be used as a general guide to investing or as a source of any specific investment recommendation. This material does not constitute legal, tax, or investment advice, nor is it a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. In preparing this material, RVC has relied upon data supplied by third parties. RVC does not undertake any obligation to update the information contained herein in light of later circumstances or events. RVC does not represent the information herein is accurate, true or complete, makes no warranty, express or implied, regarding the information herein, and shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use. This material is subject to a more complete description and does not contain all of the information necessary to make any investment decision, including, but not limited to, the risks, fees and investment strategies of an investment. All investments carry a certain degree of risk, including the possible loss of principal. There is no assurance that an investment will provide positive performance over any period of time. There are specific risks that apply to investment strategies. Since no one investment style or manager is suitable for all types of investors, this site is provided for informational purposes only. The statements contained herein are the opinions of RVC. This site contains no investment advice or recommendations. Individual investor results will vary. Rareview Capital LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Past performance is no guarantee of future results.