Why We Are Not Afraid Of Higher Yields

by Neil Azous, Chief Investment Officer

Summary

- The response to the buildup of the Federal Reserve’s balance sheet – aka Quantitative Easing – provides a road map for the response to the unwind of it.

ABC - The pace and unwind of the balance sheet should keep interest rates lower and the yield curve flatter – or benefit holders of fixed income securities.

ABC - Our model-driven approach shows that the Federal Reserve is done raising interest rates after the June FOMC meeting.

ABC - Municipal bond closed-end funds, which tend to have a longer duration profile, and are trading at wide discounts to their net asset values on a relative basis, merit an overweight allocation.

ABC

The winding down of the Federal Reserve’s balance sheet is a very contentious topic. The reason for that is because no central bank in history has ever exited from “extraordinary policies” of asset purchases. The Fed will be the first to try. Because there is no simple road map for investors to follow an opportunity exists in the fixed income market.

Balance Sheet

For this process, there are three different variables to consider for US interest rates: 1) The pace of decline in the Fed’s excess reserves, 2) broad money supply growth, and 3) which assets are most vulnerable to a running down of the balance sheet.

Fed’s Excess Reserves

The first chart below is of the year-on-year growth rate of excess reserves of the Fed’s balance sheet relative to the 5/10-year slope of the US Treasury curve. As you can see, as the Fed stopped purchasing bonds after its third QE program, the curve flattened dramatically.

ABC

ABC

Additionally, as the Fed has held its level of asset purchases static, the amount of excess reserves – or money – in the banking system continues to decline as new currency is created. Ultimately, the year-over-year rate of change in the slope of the 5/10-year US Treasury yield curve, the part most reflective of the inflation risk priced into the market, has remained at zero or lower since the Fed completed tapering their asset purchases in October 2014.

Money Supply Growth

Since the Fed stopped purchasing assets in late 2014, money supply growth has been at-or-near zero as the Fed was the marginal supplier of credit to the banking system. Additionally, loan growth, and overall credit growth has fallen to near zero. The fact that other global holders of reserves – namely China, OPEC-members countries, and Asian emerging market countries – were also running down their supply of reserves on account of US dollar strength or Federal Reserve interest rate hikes, has not helped matters either.

Asset Class Vulnerability

We believe the asset most vulnerable to the Fed running down its balance sheet is agency mortgage-backed securities (MBS), specifically their spread to US Treasuries with similar duration.

Currently, the Fed, a price insensitive owner, holds about 30% of the entire agency MBS market. As a result, during QE, other holders of MBS have received the benefit of the Fed reducing downside risks associated with MBS, such as extension risk, or “negative convexity, when interest rates undergo a cyclical change in a short period. If, and when, the Fed begins to leave the market, the Fed may reinject that risk, causing spreads to widen.

Conversely, we believe US Treasuries are much less vulnerable to the Fed running down its balance sheet.

From a mechanical perspective, when the Fed does begin to run down its balance sheet, the holder of the Fed’s reserves – mostly banks – will have to replace those reserves with US Treasuries.

Applying that process to supply and demand dynamics, the drawdown of the Fed’s balance sheet will essentially be a transfer of ownership from one price insensitive holder to another.

Conclusion: Collectively, when you drain liquidity and high-quality assets from the financial system, that it is a tightening of financial conditions. At the same time, because there is no seller of US Treasuries, only a transfer from the Fed to banks, what you are left with is a potentially flatter yield curve and a lower absolute level of long-term interest rates.

A Model Driven Approach To The Federal Reserve

Next, it is most important to know what the market expects to happen in the future relative to our expectations. A prediction, or forecast, of the 10-year Treasury yield is meaningless unless we know what that expectation is relative to the market’s, and how realistic it is that the path may evolve between now and then.

Using our Federal Reserve model, we can “digitally” recreate every single scenario that is priced into the US interest rate market. The ability to recreate the expectations embedded in the US Treasury yield curve with precision is very powerful when it comes to asset allocation, and most importantly whether the risk is greater of higher or lower interest rates.

Currently, the market is pricing a rolling “one and doneism.” This is when the market is nearly certain the next interest rate hike by the Fed – in this case, June – will be the last for the cycle. The technical term is an “inverted term structure of probabilities.”

To give you an example, according to the pricing in the market, the probability that the FOMC raises interest rates at the June FOMC meeting is 93%. However, for the September meeting (or any other), it is about 28% or lower.

Worded differently, the ratio of the unconditional probability for a June interest rate hike relative to a September (or any other) hike is greater than 3-to-1.

ABC

ABC

The magnitude of this “one and doneism” has not been priced this extreme since the March-June 2006 period at the end of the last Fed tightening cycle.

Given what we have described above, we believe there is little risk of measurably higher interest rates induced by either Fed policy or due to the underlying growth and inflation fundamentals.

With the Fed funds rate most likely reaching 1.25% this month, the Fed is coming closer to a neutral policy stance. The real neutral rate of interest by the Fed’s measurements is around zero, and the annual rate of inflation should average a little more than 1% for the remainder of the year.

While there is the potential risk for another interest rate hike at some point in the next six months, it is likely that it will be removing long-term inflation risk from the US Treasury market and flattening the yield curve further. Additionally, any move by the Fed to run down the balance sheet should depress long-term interest rates and keep the yield curve flat.

Otherwise, the only other risk that we can foresee to cyclically higher interest rates is from fiscal policy, on account of a tax cut or infrastructure plan passing in 2017. Currently, that appears to be a low probability.

Conclusion: With the market already discounting the Fed raising rates next week and then being done, unless new information in the future changes our outlook, we believe there is justification to be overweight interest rate-sensitive instruments, including longer duration fixed income.

How This Applies To Closed-End Funds

Armed with this information, how do we construct a multi-asset portfolio in the context of knowing what interest rates are pricing relative to the future?

At Rareview Capital, we use closed-end funds as our primary investment vehicle because they can potentially deliver returns through three different channels: capital appreciation, income, and the narrowing of a fund’s discount to its net asset value (NAV).

As a way of background, two-thirds of the closed-end fund universe is fixed income oriented. Also, municipal bonds make up roughly one-third of the assets in the closed-end fund market. Historically, we have found that changes in interest rates explain close to 99% of all movements in broad municipal bonds over the intermediate-term.

So, when it comes to investing in closed-end funds, we believe the ability to forecast interest rate risks in a model-driven way is very important.

Potential Benefit of a Discounted Yield

One of the key reasons why closed-end Funds have long been valued is because that in addition to owning high-yielding instruments, you are most often able to purchase them at a discount to their net asset value (NAV).

So, while the funds may pay out the income they earn from their underlying investments at the NAV price, if a fund has a discount, there is the potential benefit from an additional pickup in yield.

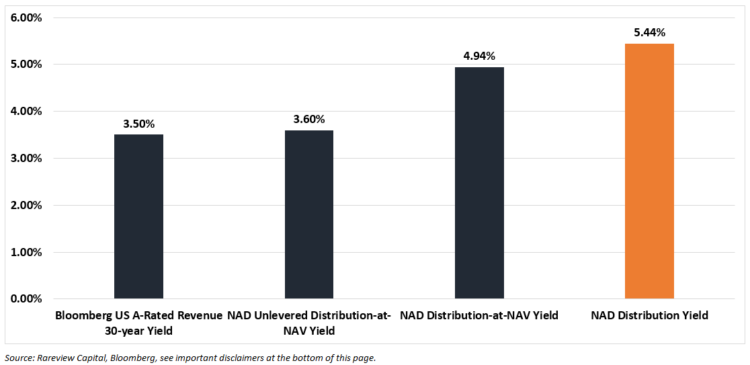

For an overview of how this adds incremental yield to a portfolio, see the below chart. The closed-end fund we reference is the Nuveen Quality Municipal Income Fund (symbol: NAD).

Bar 1: Represents the Bloomberg benchmark yield for A-rated 30-year municipal revenue bonds.

Bar 2: Represents the un-levered distribution-at-NAV yield of the Nuveen Quality Municipal Income Fund (symbol: NAD), which is roughly the equivalent of the benchmark yield.

Bar 3: Is the distribution-at-NAV yield, including the 1.37x leverage the Fund uses, which brings the yield up to 4.94%.

Bar 4: Is the distribution yield at the stock price you could buy it.

Now that you’ve included the fund’s leverage and its discount, you bring the yield all the way up to 5.45%, which is more than 1.55x the un-levered benchmark yield.

ABC

Overweight Municipals

Currently, in the closed-end fund universe, when looking at fund discounts, we find that the municipal bond asset class is currently valued the cheapest across all asset classes and regions.

As we sketched out above, the ability to purchase an asset at a discount is highly valued in the investment world. It is even more beneficial when the NAV price is readily available each day, as in this case.

Add in our model-driven approach for whether there is justification to hold more interest rate sensitive assets and we believe there is scope to be overweight municipal bond closed-end funds.

Disclaimer

This material is for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any investment or any other security, including any investment with Rareview Capital LLC (“RVC”) or any of its affiliates or any other related investment advisory services. This material is not designed to cover every aspect of the relevant markets and is not intended to be used as a general guide to investing or as a source of any specific investment recommendation. This material does not constitute legal, tax, or investment advice, nor is it a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. In preparing this material, RVC has relied upon data supplied by third parties. RVC does not undertake any obligation to update the information contained herein in light of later circumstances or events. RVC does not represent the information herein is accurate, true or complete, makes no warranty, express or implied, regarding the information herein, and shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use. This material is subject to a more complete description and does not contain all of the information necessary to make any investment decision, including, but not limited to, the risks, fees and investment strategies of an investment. All investments carry a certain degree of risk, including the possible loss of principal. There is no assurance that an investment will provide positive performance over any period of time. There are specific risks that apply to investment strategies. Closed-end funds frequently trade at a discount to their net asset value. These risks should be reviewed carefully before taking any investment action. Since no one investment style or manager is suitable for all types of investors, this site is provided for informational purposes only. The statements contained herein are the opinions of RVC. This site contains no investment advice or recommendations. Individual investor results will vary. Rareview Capital LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Past performance is no guarantee of future results.

ABC

Products or Terminology

- Nuveen AMT-Free Quality Municipal Income Fund (symbol: NAD): Securities offered through Nuveen Securities, LLC, a subsidiary of Nuveen, 333 W. Wacker Drive, Chicago, IL 60606. Nuveen is an operating division of TIAA Global Asset Management. TIAA Global Asset Management provides investment advice and portfolio management services through TIAA and its affiliated registered investment advisers. Returns quoted represent past performance which is no guarantee of future results. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Current performance may be higher or lower than the performance shown. Total returns for a period of less than one year are cumulative. Returns without sales charges would be lower if the sales charges were included. Returns assume reinvestment of dividends and capital gains. For performance current to the most recent month-end visit nuveen.com or call 800.257.8787.

- Net Asset Value (NAV): A mutual fund’s price per share or exchange-traded fund’s (ETF) per-share value. In both cases, the per-share dollar amount of the fund is calculated by dividing the total value of all securities in its portfolio, less any liabilities, by the number of fund shares outstanding.

ABC - Duration: Duration is a commonly used measure of the potential volatility of the price of a debt security, or the aggregate market value of a portfolio of debt securities, prior to maturity. Securities with a long duration generally have more volatile prices than securities of comparable quality with a shorter duration.