Investing During the Specter of War

by Neil Azous, Chief Investment Officer

Summary

Human emotion is a dominant factor when making investment decisions. This is especially true regarding military conflict, including the specter of war with North Korea. As stewards of capital, it is prudent to a have a framework in advance if military action materializes. To further contain emotion, it is also responsible to know the historical facts and the decision-making process that the professional investment community undergoes.

Below we lay out the historical facts, and our pre-determined game plan.

Consensus View

Among geopolitical think tanks, former high-level military personnel at consulting firms, independent service providers in the investment research business, or bank research departments, we believe the consensus view regarding the specter of war with North Korea is as follows:

- North Korea’s missile and nuclear weapons program is a major threat to regional stability, U.S. security and nuclear non-proliferation.

ABC - The possibility of armed conflict has risen given North Korea’s stockpile of nuclear weapons, a nuclear test, missile launches over Japan, an intense propaganda campaign, and a war of words.

ABC - The chance of misstep or miscalculation has risen.

ABC - There could be limited military action, including the shooting down of missiles.

ABC - Should the US stage an attack, there is a non-negligible probability that tactical nuclear weapons are used to decapitate North Korean leadership and command control. The justification for the use of nuclear weapons is that the game has now changed because North Korea is believed to have at least 20 nuclear weapons.

But that is where the concerns end. The costs of all-out war are too high on all sides.

Instead, the majority is split between a diplomatic solution through applying intensifying peaceful pressure, either via further sanctions or with the help of China, or learning to live with a nuclear-armed North Korea that has delivery capability via an ICBM.

Despite anxiety over the specter of war, investors share the same consensus view as firms who are paid to forecast for a living. They continue to execute their investment process knowing the starting point for any sell-off in US equities is an all-time high, frothy valuations, and extended positioning.

So, why have investors continued to go about their business as usual and place North Korea off to the side in a tail risk bucket? Put another way, why is North Korea risk not high enough to deter investors from remaining fully invested?

The pedestrian answer is that reacting to fear over a geopolitical crisis is not new. There are plenty of examples in recent years alone. Investors have contended with Russia’s annexation of Crimea and intervention in Ukraine, the rise of ISIS in Syria and Iraq following the Arab Spring, the Syrian civil war, China’s dispute with Japan over the Senkaku Islands, and the Eurozone crisis.

We think it is because sophisticated investors have gone through the below exercise and constructed a game plan.

Three Tests

To begin, it should be noted that the methodology we sketch out below is not original. It has been in practice for decades and is our default exercise upon any new geopolitical crisis.

The first step in analyzing a geopolitical crisis is to decide if the event could be systemic, or any external bleeding can be stitched up fast. Stated differently, we want to know if the event can feed on itself or if it could subside quickly.

To answer that question, we implemented the following three tests.

Historically, if the answer to the following three tests is “no” the default action by professional investors is to treat any sell-off in risky assets as a buying opportunity. That appears to be the case over the last several months regarding North Korea. Each new escalation was followed by shallower sell-offs in assets that would have the most sensitivity to a conflict, namely the Dollar-Yen (USD/JPY).

For example, the impact on August 10th was -0.79%, but the impact on Aug 28th, while intense overnight, on a closing basis was negligible, and on September 3rd the atomic test was -0.48%. Finally, the missile test in mid-September was accompanied by next-to-no market reaction.

The three tests are:

- Is there a superpower involved and is its sovereign soil at risk? Why? Because a superpower being involved can project power – that is, they can make their local issue a global one. Additionally, if its sovereign soil is at risk of war, it has the potential to damage both domestic and global economic activity due to them comprising a substantial percentage of global GDP.

ABC - Is global crude oil supply is involved? Why? Because a conflict in the Middle East that can cut off shipping lanes in the Suez Canal has major consequences to the global economy.

ABC - Is there a threat to the banking system? Why? Because the collapse of a major country’s credit, like the US subprime mortgage market, leads to economic anxiety and various data points can be weaved together into a global business slowdown narrative.

Let’s apply this test to the most recent example back in 2015 – Russia’s annexation of Crimea and the infringement on Ukraine sovereignty, a potential addition to NATO.

In that case, Russia passed two out of the three test questions. Russia is a superpower, and they are the largest non-OPEC producer of crude oil. However, the last time their capital markets caused a global market crisis was in the late 1990’s. Even the ~60% depreciation in the Russian ruble basket that followed the invasion of Crimea did not bleed into the rest of emerging markets like the days of old.

So why is North Korea even a tail risk if a superpower is not involved, there is no risk of a crude oil supply shock, and there is no threat to the banking system?

After all, North Korea is not a permanent member of the United Nations security council. It has not been declared that they have the delivery capability of a nuclear weapon. They import all their petroleum products. And, they have been largely cut off from the global banking system since President Bill Clinton’s term because of sanctions.

The reason why North Korea remains a tail risk is because of the new variables involved, even if those variables do not have the same impact as the traditional large ones sketched out above.

New Variables

Firstly, investors have not fully adjusted to this new matrix.

In a world that now includes terrorism, investors are forced to distinguish between the United States’ involvement in war, foreign terrorist attacks on US targets, foreign terrorist attacks on non-US targets, and standoffs.

For example, of the attacks on US sovereign soil in the last 100 years, the September 11 tragedy of 2001 led to a shooting war, as did the surprise attack on Pearl Harbor in 1941. The impact of those events had longer impact on asset prices as it directly involved the sovereign soil of the United States.

Conversely, the killings of US embassy officials in Libya, the bombing of the USS Cole, and the US Marine barracks in Beirut did not have lasting price effects on risky assets. These terrorist acts did not directly affect the US economy, and no attack was on US soil.

Secondly, we now must account for these new variables:

- Two unpredictable leaders – President Trump and Kim Jong-un.

ABC - North Korea’s proximity to China, a super-power. Would the US be comfortable with Chinese troops on the Canadian border?

ABC - The potential for mass casualty in Seoul, Pyongyang, and Tokyo.

ABC - The new psychology that an enemy State can reach and damage a US territory – Guam – for the first time, and possibly the United States. No American has lost sleep on this issue until now.

ABC

To be fair, investors also need to include offsets that balance out the above new variables.ABC

- Stabilization or emergency measures are now part of central bank toolkits that did not exist before the Global Financial Crisis.

ABC - The price of crude oil, should it bounce, is coming from a low absolute level. In fact, a shock to higher prices could positively impact credit and emerging markets, including Russia.

Closest Parallel

Currently, the closest parallel we can draw for the current standoff with North Korea is the Cuban Missile Crisis.

It is the only other time in history that US sovereign soil has been directly threatened with a nuclear weapon by a country that was not a superpower. Additionally, there was never a direct threat of a ground invasion, and only soft military measures were used such as a blockade (economic sanctions) and overflights.

Only time will tell if there is a “13-day” scare period like October 16–28, 1962.

Historical Investment Performance

Not all military conflicts are treated equally by asset classes. Assets differentiate between short and long wars, or whether military action takes place on US or non-US soil. Additionally, certain assets react differently depending upon which of the three tests highlighted above – superpower, crude oil, financial system – are realized.

For example, and not surprisingly, there are similar patterns of violent, crude oil volatility that occurred during several Middle Eastern conflicts, such as Desert Storm in 1991, the Iraq War in 2003, and the Syrian Conflict in 2011. ¹

- 1991 – Operation Desert Storm: One of the largest one-day drops in oil prices occurred on Jan. 17, 1991, the day after the United States launched an air campaign in Iraq. On that day, crude oil prices plunged 33%.

ABC - 2003 – The Iraq war: Oil prices rose steadily in the three months before fighting in Iraq began on March 19, 2003. Oil climbed nearly 40%, from $18 a barrel in early December to $25 on March 18. Oil plunged 24% in the week after President Bush issued his final ultimatum to Saddam Hussein on March 16.

ABC - 2011 -Libya: In the month before the U.S. intervention in the Libyan civil war on March 19, 2011, oil climbed 12%. Oil prices continued to rise in the first weeks of military action, but they reached a peak a month after the start of U.S. action. But they then started falling steadily, declining 24% by the time rebel forces gained control of the country four months later.

From a global macro investing perspective, we believe that the US dollar and crude oil are the ultimate drivers of asset prices and that everything else is just a byproduct of what those assets do next. That is why it is important to note that the North Korean confrontation should not directly impact crude oil prices unless it is from the demand side of the equation because of a broader conflict that causes economic weakness.

That said, the reaction in US Treasury yields could vary depending on whether the price of crude oil or the banking system is impacted. For example, if the supply of crude oil is jeopardized and prices went higher, it is likely that Treasury yields would rise as they reflected higher anticipated inflation. Conversely, if the banking system is impacted, then Treasury yields would drop as they reflected a decline in anticipated economic activity.

Of all asset classes, the historical pattern in US equities is the most recognizable.

For analysis, the Dow Jones Industrial Average (INDU Index) is the most used benchmark because historical data goes back 100 years.

Over the last 40 years, the asset price movements following US-led military operations that did not take place on US soil follow roughly the same path.

There is a short-term price drop of approximately 4% as there is an increase in fear and potential for economic disruption. This short-term drop is followed by a sharp rally in equities over the next one-to-six months that erases all the prior losses and adds 7% on average as expectations build for a higher level of economic activity. ²

These types of military operations are a good benchmark for potential conflict on the Korean Peninsula unless it involves a full-scale shooting war that includes ground troops crossing over the DMZ, or a nuclear strike on US soil, both of which are not deemed to be likely outcomes.

Non-US-led military operations that took place on or near US soil also follow roughly the same path. Going back 100 years and including the 14 shocks that date to the attack on Pearl Harbor in December 1941, the median one-day decline has been 2.4%. The shocks, which also include the September 11th terror attacks and the 1962 Cuban missile crisis, lasted eight days, with total losses of 7.4%. The market recouped its losses 14 days later. ³

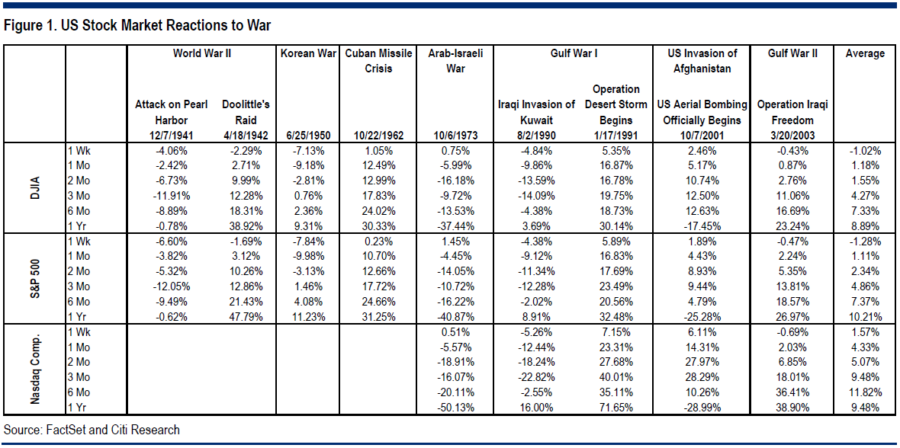

See the below table. For war on US or non-US soil, Citigroup Research offers additional information on asset price movements in response to various military actions since World War II.

The far-right column speaks for itself – on average, buying risky assets on weakness in the early stages of a conflict and holding for the intermediate-term has been a rewarding exercise following every major war.

In conclusion, we would be far more concerned about crude oil volatility than equity markets selling off based on historical precedent. Thankfully, we rest easier knowing that North Korea is an importer of crude oil and is not in close geographic proximity to any major crude oil shipping lanes.

Tail Risk Strategies

When forming a game plan for potential military or nuclear conflict we can leverage our multi-asset derivative background, and analyze the cost of implementing tail risk strategies. We determined that unless you are willing to persistently spend a meaningful percentage of your portfolio returns (i.e., ~2% annualized) implementing tail risk strategies is a sub-optimal approach to the standoff.

Specifically, we analyzed derivative structures that would benefit from:

- Higher Dollar-Won (USD/KRW) currency cross

ABC - Lower Dollar-Yen (USD/JPY) currency cross

ABC - Higher gold prices

ABC - An index sell-off in the South Korean KOSPI, Japanese Nikkei-225, and US S&P 500.

Firstly, we conclude that it is prudent to remove South Korean instruments – USD/KRW or KOSPI Index. There is a non-negligible probability that investors are not able to monetize positions, either because the markets/exchanges do not open, or banks will not make markets in local assets. This is similar to how trading shut down, and price discovery was non-existent following the Swiss National Bank removal of the Euro-Swiss (EUR/CHF) peg in January 2015. Also, the last attack on US soil on September 11th, 2001 never saw the cash stock markets open for trading until September 17th.

Secondly, we expect at least a ~8% move lower in USD/JPY as historically the first response by locals is to repatriate their money. However, owning and rolling a put option is an expensive endeavor as the timing of any event is uncertain. Additionally, while there is a way to reduce the cost of that option through exotic structures, an over-the-counter contract, or off-exchange trade, is required and not accessible to most investors. Like South Korea, there is also risk whether markets open or market-makers will be operating at that time.

Thirdly, predicting the direction of gold is cloudy at best. It is especially important to consider the quantitative analysis of gold’s historical correlations as a high degree of emotion is associated with the shiny metal. The price of gold is highly correlated to real interest rates. Therefore, if a military action is viewed with a potential disruption in economic activity, or a fall in the price of crude oil, it is probable that the price of gold will fall. Therefore, using gold call options are not a reliable tool to hedge against a possible tail risk event where it is not possible to quantify in advance what the impact may be.

Regarding equity index options, the same operational concerns exist for Japan and South Korea as currencies. That leaves US equities for global beta and the highest liquidity. Since the late 1980’s, downside option skew has been very expensive as investors systematically hedge for tail events. For example, the payoff profile for a 3-month 10% downside put option on the S&P 500 only becomes feasible on a greater than 18% index correction, unless it happened in the following 24 hours after the option was purchased. It is worth pointing out that there are various circuit breakers in place for the S&P 500 index which would stop trading for the day if it fell more than 7%. Additionally, based on historical precedent regarding war or an attack on US soil, equity markets on average do not have a drawdown of 10%.

We conclude that none of the potential rewards from these tail risk strategies justify the cost. There simply is just not enough convexity in the markets or instruments outside of Japan and South Korea as many investors already systematically hedge for tail risk, making those options very expensive. Additionally, trading directly in the markets that have the greatest sensitivity to the event comes with operational risk.

What To Watch Out For

There are some activities that we are keeping a lookout for as a catalyst to become more defensively positioned.

Firstly, if President Donald Trump reduces his public appearances. Considering that on average he has tweeted 5.5 times per day since becoming President, a sharp drop-off in activity, coincident with other factors, would indicate that military action may be prepared.

Secondly, the US Navy keeps one supercarrier group always deployed in and around the Korean Peninsula as part of its joint military efforts with South Korea. If a second carrier group is moved to the area, it would be a sign of escalation or an imminent strike against North Korea.

Thirdly, if the US Navy moves an amphibious group, including one of its hospital ships to the area, this would indicate the military is preparing for a mass casualty event due to military action. The Navy has two of these ships. The USNS Mercy is docked on the West Coast and would likely be deployed to the Korea Peninsula.

Finally, if the US Army moves some of its rapid reaction forces, such as the 101st Airborne Division, to Hawaii. It is likely that it would not be further announced that they were being sent to the Korean Peninsula, but Hawaii (or Japan) are major staging areas before a deployment to Asia.

Although additional air assets have been deployed to the Korean region, thus far we have not seen any of the developments mentioned above and believe the potential for US-initiated military action remains low.

Conclusion

We know where the consensus is in the professional investment community – that is, a military conflict initiated by North Korea is a tail risk only. There is an overwhelming bias that the standoff will result in a diplomatic solution or learn to live with a nuclear-armed North Korea.

We have answered the three test questions: 1) Is there a superpower involved, 2) Is global crude oil supply involved, and 3) Is there a threat to the banking system? The answer is “NO” to all three.

We considered modern variables that distinguish between the United States’ involvement in war, foreign terrorist attacks on US targets, foreign terrorist attacks on non-US targets, and standoffs. We conclude that the closest parallel is the Cuban Missile Crisis.

We have reviewed the historical statistics for each type of conflict, and there is a similar pattern in US equities for each conflict involving the United States, both on or off US soil. In the first one to two weeks following the event, there tends to be a sharp drawdown. However, no more than a month later, all those losses were recouped, and the equity market began to experience gains.

We have analyzed implementing various tail risk strategies and conclude that the exercise is either too expensive or the operational risk is too high to implement.

We have identified four activities that we are keeping a lookout for as a catalyst to become more defensively positioned.

Next, it is important to note that there is no precedent for what may happen if there is a pre-emptive nuclear strike of any magnitude on either the US or an allied country’s sovereign soil. It appears that the investment community is resigned to the fact that there is no hiding from that event, and hedges are too expensive to justify, so they will all perform poorly together. So, we must accept that reality and remove this concept from our primary analysis.

Armed with all this information, our investment strategy is to remain judiciously invested and be cognizant of key catalysts that may foreshadow imminent US-initiated military action. When the early warning detectors that we highlighted signal that conflict appears imminent, our goal is to raise a responsible amount of cash. We will then be able to take advantage of the historical analogs that show stocks sell off before the first shot and rise after the first shot. That way we will be prepared to buy risk assets on sharp weakness.

In the event there is military conflict, when the shooting starts, it tends to be a significant volatility-suppressing event. Counterintuitively, the stock market has historically increased because the start of war reduced the uncertainty caused by the “war risk.”

In this case, assuming the conflict is short-lived because of overwhelming US force, the market would be potentially removing the largest geopolitical risk, and the premium associated with it. This is like the Iran nuclear deal that removed the crude oil risk premium associated with blocking the Suez Canal, the major artery of crude oil delivery in the world.

At Rareview Capital we believe it is prudent to do your homework and have a game plan. Following a checklist to mitigate risk or take advantage of consistent mispricing patterns, especially regarding war, is easier than reacting to events unfolding in real-time.

We implement investment products that have a high distribution yield, trade at a discount, and can potentially mitigate volatility or recover faster. Additionally, our background in hedging solutions allows us to incorporate a risk overlay program as part of our investment process.

¹ Source: Chris Isidore, “Impact of War On Stocks and Oil,” CNN Money, 9/3/2013

² Source: HulbertRatings.com

³ Source: Adam Shell, “What Wall Street is Watching in Ukraine Crisis,” USA Today, 3/3/2014

Disclaimer

This material is for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any investment or any other security, including any investment with Rareview Capital LLC (“RVC”) or any of its affiliates or any other related investment advisory services. This material is not designed to cover every aspect of the relevant markets and is not intended to be used as a general guide to investing or as a source of any specific investment recommendation. This material does not constitute legal, tax, or investment advice, nor is it a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. In preparing this material, RVC has relied upon data supplied by third parties. RVC does not undertake any obligation to update the information contained herein in light of later circumstances or events. RVC does not represent the information herein is accurate, true or complete, makes no warranty, express or implied, regarding the information herein, and shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use. This material is subject to a more complete description and does not contain all of the information necessary to make any investment decision, including, but not limited to, the risks, fees and investment strategies of an investment. All investments carry a certain degree of risk, including the possible loss of principal. There is no assurance that an investment will provide positive performance over any period of time. There are specific risks that apply to investment strategies. Closed-end funds frequently trade at a discount to their net asset value. These risks should be reviewed carefully before taking any investment action. Since no one investment style or manager is suitable for all types of investors, this site is provided for informational purposes only. The statements contained herein are the opinions of RVC. This site contains no investment advice or recommendations. Individual investor results will vary. Rareview Capital LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Past performance is no guarantee of future results.