by Neil Azous, Chief Investment Officer

Summary

- Taking Stock

- Mid-Cycle Adjustment a False Narrative

- The Next Evolution

- Where Does This End?

- What Does This Mean For Your Portfolio?

Taking Stock

In our September 5, 2018, post “Yield Curve Inversion – What Does It Mean For Your Portfolio Right Now,” we said the Federal Reserve’s (the “Fed”) last interest rate hike for the cycle would be in December 2018. The roadmap we laid out advocated that the Fed would start cutting interest rates as soon as the summer of 2019.

Outcome: The last interest rate hike for the cycle was December 2018.

In our February 19, 2019, post “The New Narrative For Lower Interest Rates,” we double-downed on that view, reiterating that the US fixed income market continued to communicate that the Fed will likely be cutting interest rates by the end of the summer.

In our May 31, 2019, post “Fed Cutting Cycle – Our View Is Crystallized,” we illustrated that the US fixed income market was providing another key signal – when the cutting cycle will start (i.e., next three months) and end (i.e., Q4 2020-Q1 2021).

Outcome: The Fed cut interest rates at the July and September FOMC meetings.

While we are pleased to see our steadfast views come to fruition so far, what comes next is equally as important.

In today’s post, we provide supporting information that the Fed has embarked on an easing cycle that should last well into 2020.

Mid-Cycle Adjustment a False Narrative

We believe the message that the Fed is espousing – that is, the Fed is operating under the pretense of “a mid-cycle adjustment” – is a false narrative.

Historically, “mid-cycle adjustments” have been characterized as 0.75% of interest rate cuts when a short-term deceleration occurred within a longer economic expansion. These “mid-cycle adjustments” took place in 1995-96 and 1998.

Pointedly, to suggest that after 10 years of expansion, the latest interest rate cuts are a “mid-cycle adjustment” is misguided. Below we provide quantitative evidence to support our view.

To determine if monetary policy is too tight, the Fed has two preferred measures: the 3m/10y US Treasury yield curve and the 3m vs. 3m/18m USD swaps curve.

Sidebar: To see the Fed’s rationale for why they use these two measures, click HERE.

Currently, both of those curves remain deeply inverted. To identify the point where the Fed can lower the Fed funds rate such that these curves are no longer inverted, we analyze the “forward” iterations of them.

- The 3m/10y US Treasury curve is inverted out to 6 months forward (chart below for reference); The US interest rate market is priced for 0.43% of interest rate cuts over the next six months.

CEF - The 3m vs. 3m/18m forward USD swap curve is inverted out to 18 months forward (chart not referenced); The US interest rate market is priced for 0.69% of interest rate cuts over the next 18 months.

CEF

CEF

It is important to note that in the 1995-1996 and 1998 “mid-cycle adjustment” interest rate cuts, these two forward yield curves were NOT inverted leading up to the third interest rate cut.

Therefore, because the US fixed income market remains inverted, and there is another 0.43% to 0.69% of interest rate cuts discounted in the market, the Fed will need to cut no less than 0.50% more, if not 0.75%, to cause the yield curve to no longer be inverted.

Note, despite high volatility in US interest rates over the last several weeks, these expectations have not had a major shift in the past two months.

The Next Evolution

The risk to the evolution of more interest rate cuts occurring than less lies at the October 31st FOMC meeting. The market-implied probability of a 0.25% interest rate cut at that meeting is 70%.

Note, the Fed has never not cut interest rates in an easing cycle when the market probability is greater than 50% four weeks ahead of the meeting. In a tightening cycle, the threshold is higher at 70%.

Furthermore, if the Fed skips October and waits to cut in December, the FOMC will have to explain a change in course twice, rather than keeping the continuity of a cutting cycle.

Collectively, following the 0.50% of interest rate cuts by the Fed to date, and another 0.50% to 0.75% cuts required to cause the yield curve to no longer be inverted, we believe it is likely that the Fed is at the beginning of a prolonged easing cycle and not near concluding a “mid-cycle adjustment.”

Where Does This End?

The financial system does not function optimally when there is a flat or inverted yield curve for a prolonged period, like now. Therefore, a key objective of this easing cycle should be to steepen the yield curve.

Furthermore, conditions cannot be “eased” unless the Fed cuts more than what is discounted in the forward curve. This is a primary driver of our view that the Fed will ease more aggressively than the current consensus in the market.

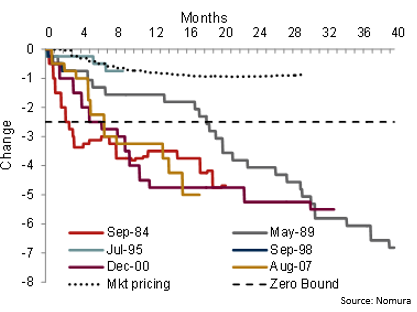

Ultimately, the fixed income market always underprices the speed and degree of Fed easing cycles, by orders of magnitudes.

For example, the dotted line on the chart to the right is the average market pricing walking into the beginning of an easing cycle. The other lines are the totality of the cuts. Many easing cycles are 4-5 times the amount priced in at the beginning.

Is it different this time?

We do not believe it is.

What Does This Mean For Your Portfolio?

It means that fixed income instruments linked to US Treasury yields are not done going up in price.

Our favored expression remains fixed income closed-end funds that stand to benefit from lower financing costs.

If you are interested in learning more about how we use our Federal Reserve model to take advantage of lower interest rates in a portfolio or make asset allocation decisions, please call us at 203-539-6067 or email us at info@rareviewcapital.com.

Disclaimer

This material is for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any investment or any other security, including any investment with Rareview Capital LLC (“RVC”) or any of its affiliates or any other related investment advisory services. This material is not designed to cover every aspect of the relevant markets and is not intended to be used as a general guide to investing or as a source of any specific investment recommendation. This material does not constitute legal, tax, or investment advice, nor is it a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. In preparing this material, RVC has relied upon data supplied by third parties. RVC does not undertake any obligation to update the information contained herein in light of later circumstances or events. RVC does not represent the information herein is accurate, true or complete, makes no warranty, express or implied, regarding the information herein, and shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use. This material is subject to a more complete description and does not contain all of the information necessary to make any investment decision, including, but not limited to, the risks, fees and investment strategies of an investment. All investments carry a certain degree of risk, including the possible loss of principal. There is no assurance that an investment will provide positive performance over any period of time. There are specific risks that apply to investment strategies. Closed-end funds frequently trade at a discount to their net asset value. These risks should be reviewed carefully before taking any investment action. Since no one investment style or manager is suitable for all types of investors, this site is provided for informational purposes only. The statements contained herein are the opinions of RVC. This site contains no investment advice or recommendations. Individual investor results will vary. Rareview Capital LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Past performance is no guarantee of future results.

Futures trading contains substantial risk of loss and is not suitable for every investor. An investor could potentially lose all or more than their initial investment. Risk capital is money that can be lost without jeopardizing ones financial security or lifestyle. Only risk capital should be used for trading and only those with sufficient risk capital should consider trading. Past performance is not necessarily indicative of future results. In light of the risks, you should undertake such transactions only if you understand the nature of the contracts (and contractual relationships) into which you are entering and the extent of your exposure to risk. Trading in futures and options is not suitable for many members of the public. You should carefully consider whether trading is appropriate for you in light of your experience, objectives, financial resources and other relevant circumstances.

Prior to buying or selling an option, investors must read a copy of the Characteristics & Risks of Standardized Options, also known as the options disclosure document (ODD). It explains the characteristics and risks of exchange-traded options. Copies are available by calling 1-888-OPTIONS, or from The Options Clearing Corporation at www.theocc.com.