by Neil Azous, Chief Investment Officer

Summary

- Background

- Gold Is Not the Portfolio Diversifier You Are Looking For

- Conclusion

Background

Let me be clear at the outset – I have no religion when it comes to contentious topics, especially gold. The yellow metal is just another commodity.

Also, the last time I formally shared my views on gold was November 2015, before negative interest rates or digital currencies became a fixture of markets.

Those views can be seen in one of the financial industry’s oldest publications – Modern Trader (formerly called Futures Magazine). The article is called “Has the golden moment passed?.”

Simply, my approach to gold is quantitative, not emotional. After regressing gold’s fundamentals, I identified seven factors that move the price of gold.

Above all else, gold is most sensitive to real US bond yields – that is, the lower that real bond yields go, the higher the gold price should go, and vice versa. Importantly, this relationship is strong in the post-Global Financial Crisis (GFC), quantitative easing era.

For example, since the peak in yields last November, the real 10-year US Treasury yield fell from 1.16% to 0.16%. In response to that 1% fall, the spot price of gold appreciated ~25% during this period.

So, like in past cycles, lower real yields are the primary driver of higher gold prices once again.

Armed with this information and the expectation that real yields should continue lower, the question arises whether gold should be added to a portfolio for diversification, including as a replacement for bonds?

The answer is that gold is not a portfolio diversifier if you have a long-term horizon. Conversely, when growth and inflation are below trend, and the Fed is in an easing cycle, such as now, gold can be added “tactically.”

Gold Is Not the Portfolio Diversifier You Are Looking For

Historically, US Treasuries are the primary instrument to diversify a portfolio because they provide stability when stocks fall for an extended period, especially during bear markets or crises.

The problem currently is that government bonds have less room to appreciate than they did in the past, and the risk of owning them is asymmetric should inflation materialize.

In the periods surrounding the last two recessions, the 10-year US Treasury yield dropped by 3.46% on average from peak-to-trough.

Therefore, interest rates would have to fall to the zero-lower bound (ZLB) – between 0.00% and 0.25% – from the current level to provide the same benefit to a portfolio as during the periods surrounding the last two recessions.

Because US Treasuries currently offer a lower coupon than what was received historically, the total return in the next recession may be lower than past downturns. Consequently, the stewards of other people’s capital should acknowledge that bonds have the potential to offer less protection in the next slump.

As a result, there is a growing debate that a new portfolio diversifier may be required, including one that does not guarantee to return principal at maturity, and that does not pay a fixed coupon.

Conventional thinking is that a potential diversifier that meets these criteria is gold.

We disagree with conventional thinking and believe replacing bonds with gold in a diversified portfolio is misguided.

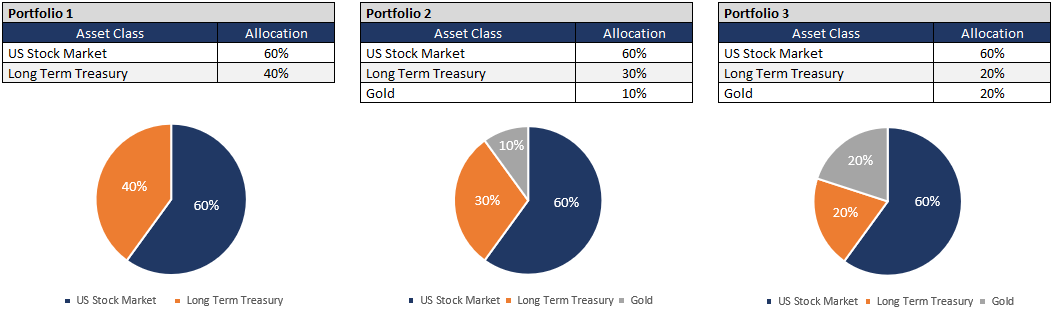

In fact, the more gold you add to a traditional 60/40 stock-bond portfolio, the worse the outcome is, especially over a long period.

Below, we backtest a hypothetical portfolio asset allocation and compare historical and realized returns and risk characteristics against various lazy portfolios.

Parameters

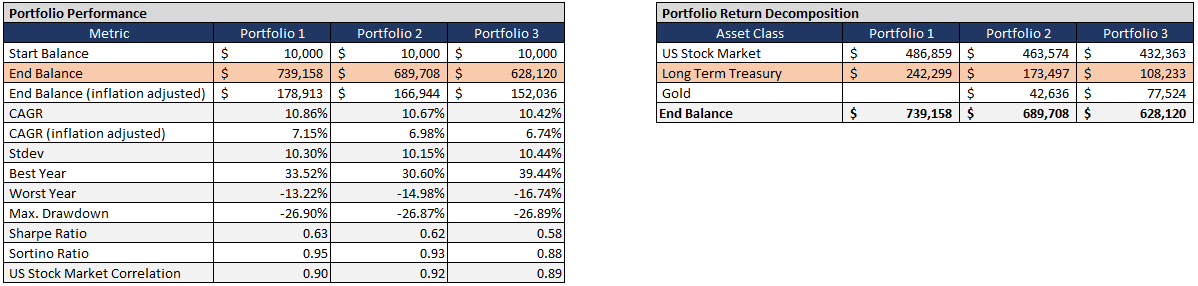

The main takeaway is that a traditional 60/40 stock-bond portfolio has a higher End Balance with similar risk characteristics relative to a 60/30/10 and 60/20/20 stock-bond-gold portfolio.

Specifically, we point you to the Portfolio Return Decomposition illustration. The lower End Balance between portfolios with reduced Long Term Treasury weightings is significant.

This difference is primarily because of the lack of compounding of dividend reinvestment income from the portion allocated to gold. If you were to add the variable costs to owning gold that are not included – a fund, futures, or physical form – the results would be even worse.

Next, contrary to the qualitative view, a portfolio with gold has mixed drawdown results during historical periods of market stress because it is treated just like any other security when asset deflation is occurring. Said differently, for all the emotion associated with gold, it’s performance is uninspiring when you think you need it most.

Finally, there is an important practical limitation to replacing bonds with gold.

If your goal is to get through retirement, not simply reach it, living off the expected potential capital gains of gold instead of receiving ordinary income systematically is a bet we believe retirees do not want to make.

Conclusion

The view on gold I articulated in November 2015 has not changed regardless of the introduction of negative interest rates and digital currencies.

The primary reason to own gold is that it appreciates when real interest rates fall, nothing more.

Forty years of empirical data show that adding gold to a diversified portfolio is less optimal than holding bonds because of the lost income stream.

Instead, investors who want to own gold as a portfolio diversifier should consider the necessity of tactically owning it during periods of lower real US interest rates and not through periods of higher real interest rates.

A simple rule of owning gold during the periods surrounding Federal Reserve easing cycles, and removing it from a portfolio during hiking cycles, could potentially increase returns for a diversified portfolio.

This benefit is because price appreciation drives most bond returns during an easing cycle and becomes a detriment during a hiking cycle. The negative cost associated with owning gold only compounds this issue.

If you want to own gold outside of an easing cycle, that is fine. Just don’t call it a portfolio diversifier or bet on it for retirement income.

Instead, own some because you are good at market-timing or navigating the contours of a Federal Reserve easing cycle. Otherwise, you are left with a crystal ball that says budget deficits, extreme central banking, or geopolitical risk will one day, in the future, drive the price of gold up. And, between now and then, you do not care about the opportunity cost of the capital you tied up.

As stated at the onset – the yellow metal is just another commodity. Everything else is fool’s gold.

If you are interested in learning about how we would tactically add gold to a portfolio or make asset allocation decisions, please call us at 203-539-6067 or email us at info@rareviewcapital.com.

Disclaimer

This material is for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any investment or any other security, including any investment with Rareview Capital LLC (“RVC”) or any of its affiliates or any other related investment advisory services. This material is not designed to cover every aspect of the relevant markets and is not intended to be used as a general guide to investing or as a source of any specific investment recommendation. This material does not constitute legal, tax, or investment advice, nor is it a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. In preparing this material, RVC has relied upon data supplied by third parties. RVC does not undertake any obligation to update the information contained herein in light of later circumstances or events. RVC does not represent the information herein is accurate, true or complete, makes no warranty, express or implied, regarding the information herein, and shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use. This material is subject to a more complete description and does not contain all of the information necessary to make any investment decision, including, but not limited to, the risks, fees and investment strategies of an investment. All investments carry a certain degree of risk, including the possible loss of principal. There is no assurance that an investment will provide positive performance over any period of time. There are specific risks that apply to investment strategies. Closed-end funds frequently trade at a discount to their net asset value. These risks should be reviewed carefully before taking any investment action. Since no one investment style or manager is suitable for all types of investors, this site is provided for informational purposes only. The statements contained herein are the opinions of RVC. This site contains no investment advice or recommendations. Individual investor results will vary. Rareview Capital LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Past performance is no guarantee of future results.

Hypothetical Performance. This post shows certain performance figures that are hypothetical in nature. Readers should understand that hypothetical performance herein has many notable limitations, including the following: (1) the model assumes a static portfolio of holdings rebalanced annually. (2) in the process of calculating the hypothetical performance shown herein, the model did not take into account trading in and out of positions within a given year; (3) in actual trading, counterparties can be expected to vary the pricing and other economic terms of the various holdings, which may vary from the pricing used to calculate hypothetical returns; (4) assumptions regarding expenses and other economic influences may prove to be materially incorrect.

- Past performance is not a guarantee of future returns.

- The entered time period is automatically adjusted based on the available return data for the specified assets

- The annual results for 2019 are based on full calendar months from January to September

- CAGR = Compound Annual Growth Rate

- Stdev = Annualized standard deviation of monthly returns

- Sharpe and Sortino ratios are calculated and annualized from monthly excess returns over risk free rate (1-month treasury bill)

- Stock market correlation is based on the correlation of monthly returns

- Drawdowns are calculated based on monthly returns excluding cashflows

- The backtested results include annual rebalancing of portfolio assets to match the specified allocation

- The results use total return and assume that all dividends and distributions are reinvested. Taxes and transaction fees are not included

- Portfolio cashflows and rebalancing for quarterly and annual periods are aligned with calendar periods

- Software and Data Source: Silicon Cloud Technologies LLC