The Case for Switching to Municipal Bond Closed-End Funds from Cash Municipal Bonds

by Neil Azous, Chief Investment Officer

Summary

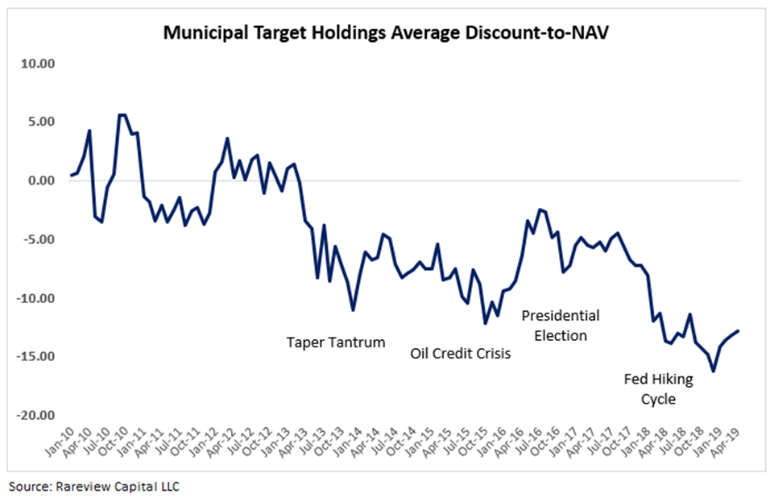

- The Starting Point – Discounts in the Municipal Bond CEF Universe Remain in the Top 10% of History

- Municipal Bond Closed-End Funds Outperform Municipal Bond Open-End Funds

- Municipal Bond Closed-End Funds Have a Higher Tax-Equivalent Yield than Other Public Income Asset Classes

CEF

Typically, once a decade, investors can take advantage of a Federal Reserve easing cycle by investing in levered vehicles that could disproportionately benefit from lower leverage costs.

We believe this is one of those opportunities and investors should consider replacing their cash municipal bond holdings with a closed-end fund (CEF) municipal bond strategy.

If leverage costs decline and distribution rates increase, there is the potential for significant discount-to-NAV tightening in addition to price appreciation.

There are four potential ways to make money in municipal bonds CEF’s:

- Price return

- Broad discount-to-NAV tightening

- Income

- Discount-to-NAV capture (i.e., alpha generation)

Periodically, two or three of those return streams line up at the same time. Historically, it is extraordinarily rare that all are aligned simultaneously. We believe this is beginning to occur now.

The Starting Point – Discounts in the Municipal Bond CEF Universe Remain in the Top 10% of History

Despite the bounce this year, in aggregate, discounts in the municipal bond CEF universe remain in the top 10% of history and could reprice as leverage costs are lowered. Therefore, if the Federal Reserve were to cut interest rates by 75-100 basis points over the next 12 months, we believe the total returns on a risk-adjusted and absolute basis would be extremely compelling.

CEF

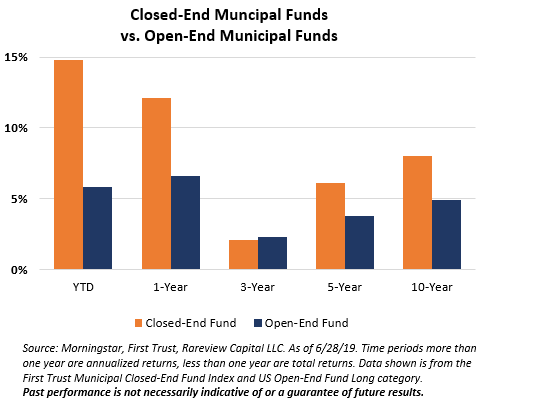

Municipal Bond Closed-End Funds Outperform Municipal Bond Open-End Funds

The below table shows the annualized performance of US closed-end municipal bond funds vs. US open-end municipal bond funds. The total return differential over short- and long-term periods in favor of municipal bond closed-end funds is meaningful. Note: Muni CEF’s typically underperform during interest rate hiking cycles as the cost of leverage increases. This is the reason why the 3-year return figure is roughly equal to that of the open-end funds.

There are three main reasons why municipal bond closed-end funds outperform municipal cash bonds over the long-term:

There are three main reasons why municipal bond closed-end funds outperform municipal cash bonds over the long-term:

- Leverage: Muni CEF’s use a moderate amount of leverage, 36% on average. This leverage helps generate a higher total yield because municipal CEF’s borrow short and invest long.

EF - Discount: Buying a CEF at a discount increases the yield. For example, if the distribution yield for a CEF is 5% at its Net-Asset-Value (NAV), but is trading at a 10% discount to its NAV, the yield you are purchasing the CEF at is 11% higher, or 5.55%. That additional yield pick-up, compounded over time, helps generate a higher total return.

CEF - Fully Invested: Because the CEF’s are closed vehicles, a portfolio manager can remain fully invested (i.e., little-to-no cash holdings) and hold bonds that may be harder to sell. Note, approximately 25% of cash municipal bonds trade on any given day. If a CEF manager can invest with the added comfort of the bonds being held to maturity, they are often able to generate excess returns over the benchmark and avoid the slippage of transaction costs, which are not insignificant in cash municipal bond trading.

CEF

Municipal Bond Closed-End Funds Have a Higher Tax-Equivalent Yield than Other Public Income Asset Classes

Muni CEF’s offer increased yield benefits because of the federal tax exemption.

The muni CEF tax-equivalent yield for the highest tax brackets is greater than other public income asset classes. Also, when adjusted for historical volatility, the yield on muni CEF’s is attractive relative to other income choices.

Finally, tax efficiency can be potentially increased by purchasing state muni CEF’s, which are exempt from state-income taxes.

CEF

Conclusion

The current profile of muni CEF’s – four potential ways to generate excess returns simultaneously during a Federal Reserve easing cycle – coupled with a higher tax equivalent yield than other public income assets argue allocating out of cash bonds or open-end mutual funds into a muni CEF strategy.

It is important to note that the primary driver of potential excess returns is not predicated on long-term Treasury yields declining, but any interest rate cuts by the Federal Reserve. Also, regardless if interest rate cuts are 75 or 225 basis points (i.e., all the way back to the zero-bound), the outperformance over a cash-bond product could be meaningful.

If you are interested in learning more about our Managed Municipal Bond (Tax-Exempt Income) Closed-End Fund separate account strategy, please call us at 203-539-6067 or email us at info@rareviewcapital.com.

Disclaimer

This material is for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any investment or any other security, including any investment with Rareview Capital LLC (“RVC”) or any of its affiliates or any other related investment advisory services. This material is not designed to cover every aspect of the relevant markets and is not intended to be used as a general guide to investing or as a source of any specific investment recommendation. This material does not constitute legal, tax, or investment advice, nor is it a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. In preparing this material, RVC has relied upon data supplied by third parties. RVC does not undertake any obligation to update the information contained herein in light of later circumstances or events. RVC does not represent the information herein is accurate, true or complete, makes no warranty, express or implied, regarding the information herein, and shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use. This material is subject to a more complete description and does not contain all of the information necessary to make any investment decision, including, but not limited to, the risks, fees and investment strategies of an investment. All investments carry a certain degree of risk, including the possible loss of principal. There is no assurance that an investment will provide positive performance over any period of time. There are specific risks that apply to investment strategies. Closed-end funds frequently trade at a discount to their net asset value. These risks should be reviewed carefully before taking any investment action. Since no one investment style or manager is suitable for all types of investors, this site is provided for informational purposes only. The statements contained herein are the opinions of RVC. This site contains no investment advice or recommendations. Individual investor results will vary. Rareview Capital LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Past performance is no guarantee of future results.

Other important risk considerations, products or terminology:

- Closed-End Fund Leverage: Leverage is a speculative technique that exposes a closed-end fund to greater risk and increased costs than if it were not used. The use o leverage may cause greater volatility in the level of a closed-end fund’s NAV, market price and distributions on its Common Shares. Leverage will also result in higher fees due to the closed-end fund manager because the amount of assets under management will be included in the closed-end funds Managed Assets. There can be no assurance that a closed-end fund will use leverage or that its levered strategy will be successful during any period in which it is employed. Additional information on how closed-end funds use leverage can be found at CEF Connect.

- Tax Risk: New federal or state governmental action could adversely affect the tax-exempt status of securities held by a closed-end fund, resulting in higher tax liability for shareholders and potentially hurting performance as well. It is strongly suggested that investors obtain independent advice in relation to any investment, financial, legal, tax, accounting or regulatory issues discussed in this commentary.

- Net Asset Value (NAV): A mutual fund’s price per share or exchange-traded fund’s (ETF) per-share value. In both cases, the per-share dollar amount of the fund is calculated by dividing the total value of all securities in its portfolio, less any liabilities, by the number of fund shares outstanding.

- Discount-to-NAV: A pricing situation that occurs with a closed-end fund when its market price is currently lower than the net asset value of its components.

- Alpha: We determine Alpha as the relative return of a Closed-End Fund’s (CEF) share price to its Net Asset Value (NAV). Any return of the share price that is greater than the NAV is deemed to be positive alpha. Any return that is negative than the NAV is deemed to be negative alpha.

- Basis Points (BPS): One hundredth of one percent, used chiefly in expressing differences of interest rates.