by Neil Azous, Chief Investment Officer

Summary

- Taking Stock

- A Model Driven Approach To The Federal Reserve

- What Does Rareview Capital Think?

- What Does This Mean For Your Portfolio?

- Where Are We Wrong?

Taking Stock

In our September 5, 2018, post “Yield Curve Inversion – What Does It Mean For Your Portfolio Right Now,” we said the following:

- The Federal Reserve’s last interest rate hike for the cycle would be in December 2018.

- The risk of principal loss in fixed income assets over the intermediate-term was de minimis.

Currently, there are no more interest rate hikes priced into US fixed income markets and US Treasury yields are notably lower than they were at the beginning of September.

To support those conclusions, we provided our framework for the different phases of yield curve inversion in the US fixed income markets, and what those historically indicated would happen in the future regarding Federal Reserve interest rate policy.

The roadmap we laid out advocated that we could enter Phase 4 – when the Federal Reserve starts cutting interest rates – as soon as the summer of 2019.

None of the views we sketched out in September are different today. In fact, with six months passing, many views have been validated, or are close to fruition.

A Model Driven Approach To The Federal Reserve

It is important to know what the market anticipates happening in the future relative to current expectations. Said differently, a prediction or forecast of the 10-year Treasury yield is meaningless unless we know what that expectation is relative to the market’s, and how realistic it is that the path may evolve between now and then.

Using our Federal Reserve model, we can “digitally” recreate various scenarios that are priced into the US interest rate market. The ability to recreate the expectations embedded in the US Treasury yield curve with precision is a very powerful tool to determine the direction of interest rates, either higher or lower. Those conclusions are a critical component for our asset allocation decisions.

So, what is our Federal Reserve super-forecasting model saying now?

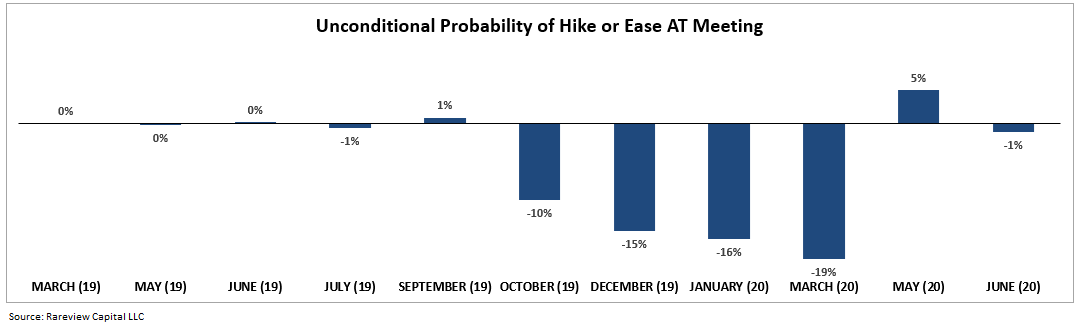

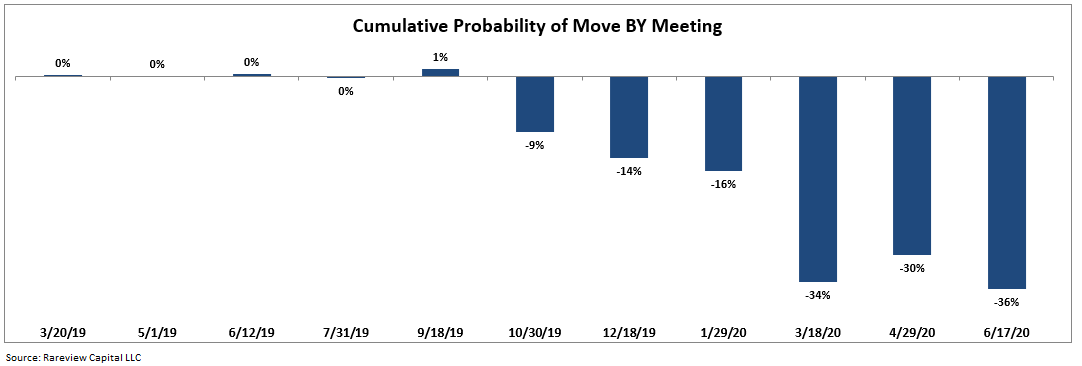

Below are two bar charts.

The first illustration shows the unconditional probabilities of an interest rate move, either hike or cut, “AT” a certain meeting.

The second illustration shows the cumulative probabilities for an interest rate move, either hike or cut, “BY” a certain meeting.

The key takeaways are:

- The probability for an interest rate hike “AT” the March FOMC meeting is less than zero (first chart).

- The market “cumulatively” is not pricing in an interest rate hike in all of 2019 (second chart).

- The market is now pricing interest rate cuts (i.e., 20-40 bps), starting as soon as the fourth quarter of 2019.

Collectively, the market is pricing the Federal Reserve shifting into an easing cycle over the next 12 months.

As a yardstick, statistically, following the end of past interest rate cycles, the Federal Reserve, on average, has begun cutting interest rates 182 days after the last interest rate hike, which could put the first interest rate cut as early as June. Note, the Fed has never cut interest rates within five months since the last hike, but it has been as long as 12 months.

Finally, while the Fed’s “Dot Plot” calls for two interest rate hikes in 2019, we think the relevance of this forward guidance tool has shrunk dramatically now that the Fed is in a neutral policy stance.

Currently, the difference between those who bet for a living and those who have a Ph.D. is two interest rate hikes. Investors believe that at the March FOMC meeting the Federal Reserve will more closely align with the market, and the “Dot Plot” will be reduced to one hike in 2019.

What Does Rareview Capital Think?

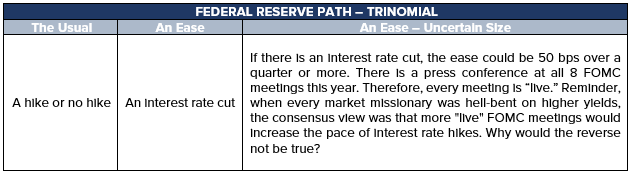

For most of the interest rate hiking cycle, market professionals have operated in a “binomial” world, or a path of policy that consisted of two outcomes – a hike or no hike.

Now, the environment has shifted to a “trinomial” world, or a path of policy that consists of three outcomes – a hike, no hike, or cut.

That said, it is challenging to qualitatively implement the shift to a “trinomial” from a “binomial” world in a portfolio. After all, it is not easy to transition a portfolio to this sequence: when does the Fed stop hiking…to…if the Fed pauses…what comes next…a cut…and how much and how fast?

To guide you, below is a table and explanation of the new “trinomial” world investors live in.

While it is common practice for the Federal Reserve to raise interest rates by 25 bps at a time, it is equally as rare for them to cut by 25 bps at a time.

Therefore, it is probable that the first interest rate cut could be 50 bps, or 25 bps cuts could happen in rapid succession. For example, the Fed could cut interest rates by a total of 150-200 bps at four meetings in a row. The difference now with a press conference at every FOMC meeting, not just quarterly when forward guidance existed, is that the 150-200 bps of cuts could also occur in a short-time span – i.e., 6 to 12 months.

Also, it is prudent to model increased probabilities for an inter-meeting interest rate cut in case there is an exogenous shock. For example, in all easing cycles going back to 1980, the Federal Reserve cut interest rates in between meetings in response to surprise market turmoil – Global Financial Crisis, Dot.com blow-up, Long-Term Capital Management, etc.

All in all, the third outcome – An Ease – Uncertain Size – is where the most asymmetry in the market exists.

Using our Federal Reserve super-forecasting model, we can easily transition from one phase to another, and take advantage of opportunities that arise, or avoid pitfalls, in this new “trinomial” world.

What Does This Mean For Your Portfolio?

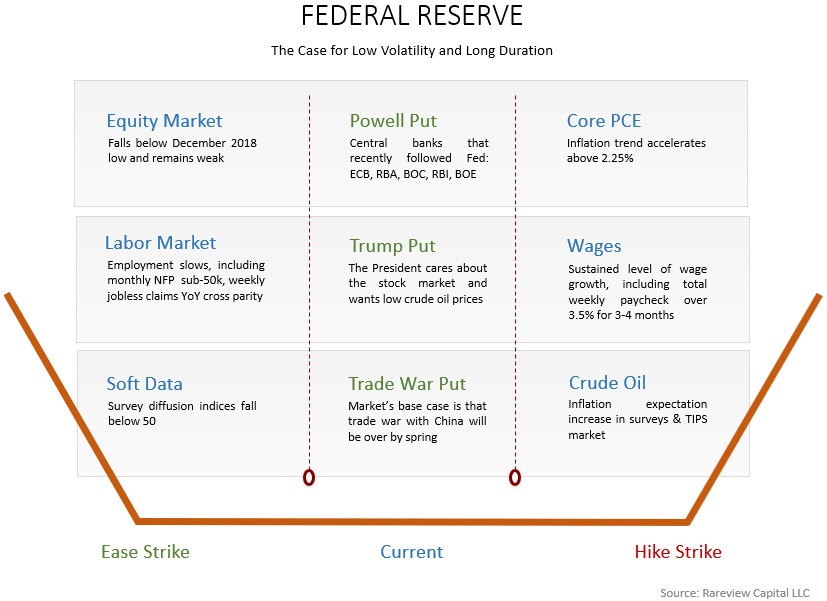

Below is an illustration in the form of an option strangle that captures the market’s current mindset. It shows the break-even points that could potentially lead to an ease (left column) or hike (right column).

Currently, in isolation or in aggregate, there is not enough supporting evidence for the option strike to move in-the-money in either direction. However, based on the pricing in fixed income, it is closer to the “ease” strike. That is because the “hike” strike is now foremost predicated on inflation as evidenced from the most recent communications by various Federal Reserve members.

Based on the market pricing showing no action by the Federal Reserve between now and June, and the factors that generally drive a hike or cut not being strong enough currently, investors should be biased to collect positive carry in fixed income and not be underweight.

If you are sensitive to that being “it” for yields or the Fed funds rate going higher, it is prudent to right size your portfolio, including adding duration. For example, after the end of every Federal Reserve interest rate hiking cycle, the 30-year US Treasury yield has tended to fall below the effective Fed funds rate, which is currently at 2.4%. While we do not think the case is as strong in this cycle considering the lower absolute level of yields, the gap between the current 30-year yield and the Fed funds rate is still very wide.

Where Are We Wrong?

The market psychology today is different than last September when loose financial conditions, primarily driven by high equity prices and tight credit spreads, was the main factor for continued interest rate hikes.

Also, historically, once the Federal Reserve stopped raising interest rates, never once have they restarted them. The next action has always been an interest rate cut.

That said, we respect that each cycle is unique, and a modern Federal Reserve may be different from one 25 years ago. Therefore, it is prudent to identify where we are wrong.

Today, above all other inputs, we believe higher inflation, if it were to materialize, could potentially negate the framework sketched out above and lead to the Federal Reserve raising interest rates after pausing at the March FOMC meeting.

Note, if the Fed skips raising interest rates at the March FOMC meeting, the conditions for resuming interest rate hikes at any meeting later differ from the criteria from the previously measured pace of hikes.

Put another way, continuing a sequence requires that the baseline expectations of that pattern not be materially different. That does not mean it is impossible to resume interest rate hikes. It suggests the criteria are not the same as those that produced the December hike after the September hike – that is, loose financial conditions.

That criteria, in our opinion, is inflation remaining at or above the Federal Reserve’s symmetrical target range of 1.80% to 2.2% on a sustained basis (i.e., 3-6 months).

Conclusion

Absent a durable bout of inflation materializing, we believe the US fixed income market is communicating that the Federal Reserve will likely be cutting interest rates by the end of the summer, or nine months following the last hike.

As a result, over the next 12 months, the risk is significantly lower yields across the curve.

Also, after 18-months, the general negative sentiment towards income-oriented assets from being in a “rising interest rate environment” has ended.

Now, we believe income wins under market conditions in which fixed income volatility is contained, and the Fed is responsive to deteriorating economic conditions.

If you are interested in learning more about how we use our Federal Reserve model to take advantage of lower interest rates in your portfolio or for your clients, please call us at 203-539-6067 or email us at info@rareviewcapital.com.

Disclaimer

This material is for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any investment or any other security, including any investment with Rareview Capital LLC (“RVC”) or any of its affiliates or any other related investment advisory services. This material is not designed to cover every aspect of the relevant markets and is not intended to be used as a general guide to investing or as a source of any specific investment recommendation. This material does not constitute legal, tax, or investment advice, nor is it a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. In preparing this material, RVC has relied upon data supplied by third parties. RVC does not undertake any obligation to update the information contained herein in light of later circumstances or events. RVC does not represent the information herein is accurate, true or complete, makes no warranty, express or implied, regarding the information herein, and shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use. This material is subject to a more complete description and does not contain all of the information necessary to make any investment decision, including, but not limited to, the risks, fees and investment strategies of an investment. All investments carry a certain degree of risk, including the possible loss of principal. There is no assurance that an investment will provide positive performance over any period of time. There are specific risks that apply to investment strategies. Closed-end funds frequently trade at a discount to their net asset value. These risks should be reviewed carefully before taking any investment action. Since no one investment style or manager is suitable for all types of investors, this site is provided for informational purposes only. The statements contained herein are the opinions of RVC. This site contains no investment advice or recommendations. Individual investor results will vary. Rareview Capital LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Past performance is no guarantee of future results.

Futures trading contains substantial risk of loss and is not suitable for every investor. An investor could potentially lose all or more than their initial investment. Risk capital is money that can be lost without jeopardizing ones financial security or lifestyle. Only risk capital should be used for trading and only those with sufficient risk capital should consider trading. Past performance is not necessarily indicative of future results. In light of the risks, you should undertake such transactions only if you understand the nature of the contracts (and contractual relationships) into which you are entering and the extent of your exposure to risk. Trading in futures and options is not suitable for many members of the public. You should carefully consider whether trading is appropriate for you in light of your experience, objectives, financial resources and other relevant circumstances.

Prior to buying or selling an option, investors must read a copy of the Characteristics & Risks of Standardized Options, also known as the options disclosure document (ODD). It explains the characteristics and risks of exchange traded options. Copies are available by calling 1-888-OPTIONS, or from The Options Clearing Corporation at www.theocc.com.

Index Descriptions, Products, or Terminology:

- Duration: A measure of the sensitivity of the price – the value of principal – of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years