by Neil Azous, Chief Investment Officer

Last year, nearly every asset class fell, with many experiencing a bear market decline of more than 20%. The damage done to closed-end funds was significant, including, what we believe, was an extreme degree of tax loss selling in December. In 2018, the discount-to-NAV widened in ALL sectors. The last time that occurred was 2008.

This is your closed-end fund specialist tapping you on the shoulder. If you require income and want the potential to generate alpha, closed-end funds should be part of any asset allocation shifts you make in the new year. The potential for alpha generation and higher-than-normal total returns in closed-end funds is one of the best opportunities we have ever seen.

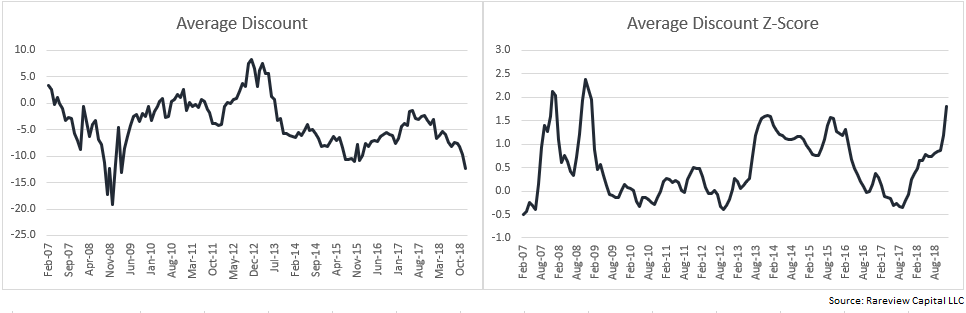

The aggregate discount-to-NAV for our target universe of closed-end funds is the second widest on record, just behind the Global Financial Crisis. The below two charts show the absolute level of discounts and their relative cheapness in z-score terms for our target universe.

Now, to be clear, we are not advocating that you buy a closed-end fund index product or a handful of securities that you are familiar with. Despite the opportunity, this is not an exercise where you throw a dart at the board and close your eyes. We believe asset allocation, sector selection, and weightings are imperative.

We expect last year’s challenging market environment to continue, including the long-lived credit cycle ending and the Federal Reserve transitioning to an easing from hiking cycle.

A strategy that seeks to generate income in excess of the risk-free rate is required to generate a positive total return. This approach is available from active managers, such as us.

That said, an active manager should be able to demonstrate that they can generate positive alpha from discount-capture in a bull market and show less discount widening than a benchmark in a bear market.

Our active management approach to closed-end funds – tactical asset allocation, model-driven valuation, and risk management – met that criteria in 2017 when volatility reached a record low and in 2018 when volatility was extremely elevated.

Call Rareview Capital at 203-539-6067, to learn how we plan to take advantaging of the best opportunity in closed-end funds since the Global Financial Crisis.

Disclaimer

This material is for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any investment or any other security, including any investment with Rareview Capital LLC (“RVC”) or any of its affiliates or any other related investment advisory services. This material is not designed to cover every aspect of the relevant markets and is not intended to be used as a general guide to investing or as a source of any specific investment recommendation. This material does not constitute legal, tax, or investment advice, nor is it a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. In preparing this material, RVC has relied upon data supplied by third parties. RVC does not undertake any obligation to update the information contained herein in light of later circumstances or events. RVC does not represent the information herein is accurate, true or complete, makes no warranty, express or implied, regarding the information herein, and shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use. This material is subject to a more complete description and does not contain all of the information necessary to make any investment decision, including, but not limited to, the risks, fees and investment strategies of an investment. All investments carry a certain degree of risk, including the possible loss of principal. There is no assurance that an investment will provide positive performance over any period of time. There are specific risks that apply to investment strategies. These risks should be reviewed carefully before taking any investment action. Since no one investment style or manager is suitable for all types of investors, this site is provided for informational purposes only. The statements contained herein are the opinions of RVC. This site contains no investment advice or recommendations. Individual investor results will vary. Rareview Capital LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

There are risks inherent in any investment including the possible loss of principal. There can be no assurance that separate account objectives will be achieved. Closed-end funds are traded on the secondary market through one of the stock exchanges. A funds investment return and principal value will fluctuate so that an investor’s shares may be worth more or less than the original cost. Shares of closed-end funds may trade above (a premium) or below (a discount) the net asset value (NAV) of the fund’s portfolio. There is no assurance that a Fund will achieve its investment objective. Past performance does not guarantee future results.

Index Descriptions, Products, or Terminology:

- Net Asset Value (NAV): A mutual fund’s price per share or exchange-traded fund’s (ETF) per-share value. In both cases, the per-share dollar amount of the fund is calculated by dividing the total value of all securities in its portfolio, less any liabilities, by the number of fund shares outstanding.

- Discount-to-NAV: A pricing situation that occurs with a closed-end fund when its market price is currently lower than the net asset value of its components.

- Alpha: A risk-adjusted measure of an investment’s excess return relative to a benchmark.

- Z-Score: The number of standard deviations from the mean a data point is.