Why We Are Still Not Afraid Of Higher Yields

by Neil Azous, Chief Investment Officer

Summary

- The Current Market Mind Map

- Where We Are At In The Interest Rate Hiking Cycle

- What Is Our Federal Reserve Model Saying?

- What Does Rareview Capital Think

- Yardstick #1 – Terminal Rate

- Yardstick #2 – Neutral Rate

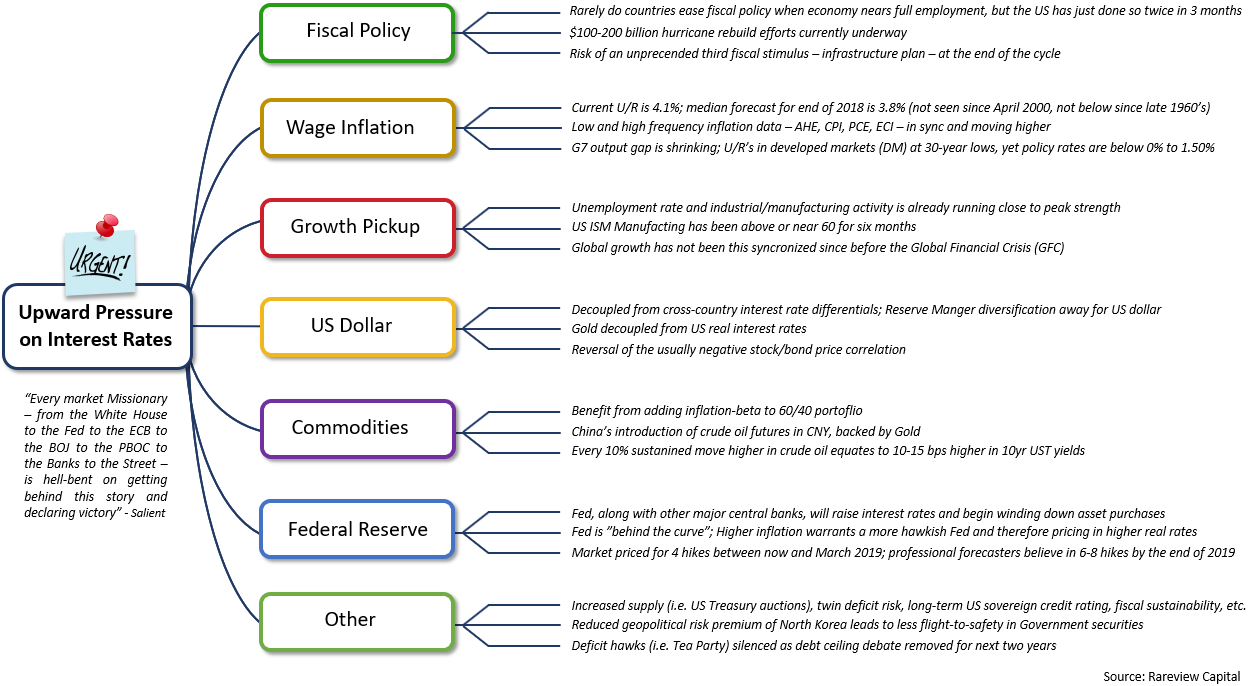

The Current Market Mind Map

A Mind Map is a visual representation of hierarchical information that includes a central idea surrounded by connected branches of associated topics. In a Mind Map, information is structured in a way that mirrors exactly how the brain functions – in a radiant rather than linear manner. A Mind Map literally ‘maps’ out your thoughts, using associations, connections and triggers to stimulate further ideas.

Currently, upward pressure on interest rates is the central idea and every day it feels like the market is adding to the narrative.

Here is the current Mind Map of the market regarding higher interest rates.

While a Mind Map is a great tool for brainstorming new ideas, its unstructured format allows ideas and thoughts to flow freely, rather than forcing them down into a utility that can be used for portfolio construction. Exactly at times like this it is incumbent upon stewards of other people’s capital to create a working framework and follow a process to reduce jumping around among topics.

Also, a Mind Map is an illustration of the past or present, not the future. Worded differently, it is most important to know what the market expects to happen in the future relative to expectations. A prediction, or forecast, of the 10-year US Treasury yield is meaningless unless we know what that expectation is relative to the market’s, and how realistic it is that that the path may evolve between now and then.

Using our Federal Reserve model, we can “digitally” recreate various scenarios that are priced into the front-end of the US interest rate market. The ability to recreate the expectations embedded in the US Treasury yield curve with precision is very powerful when it comes to asset allocation, and most importantly whether the risk is greater of higher or lower interest rates.

This model emphasizes our process-driven approach to investing. It is at the very heart of everything we do here at Rareview Capital, and we have spent considerable time developing it.

Below, we use our Federal Reserve Model to take the market’s Mind Map and turn it into a working framework.

Ultimately, despite the Mind Map, we find that we are not afraid of higher interest rates as this hiking cycle is well-discounted in the marketplace currently. Otherwise, we at least know where we are wrong.

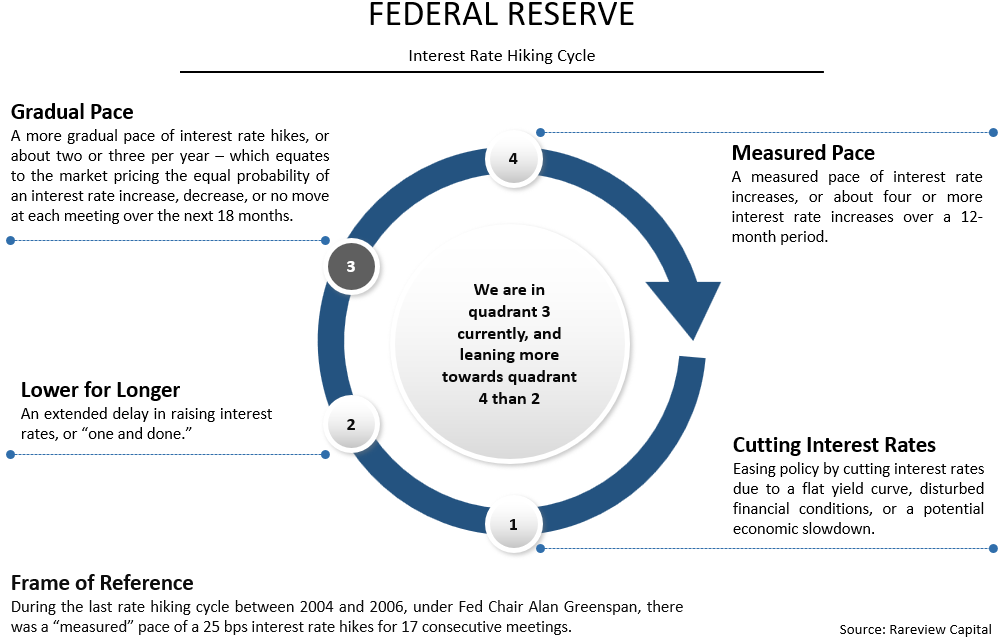

Where We Are At In The Interest Rate Hiking Cycle

Look at this simple grouping. The interest rate hike story can be put into four quadrants. Here’s how we think about each one:

Currently, the market is oscillating somewhere between quadrant 3 and 4.

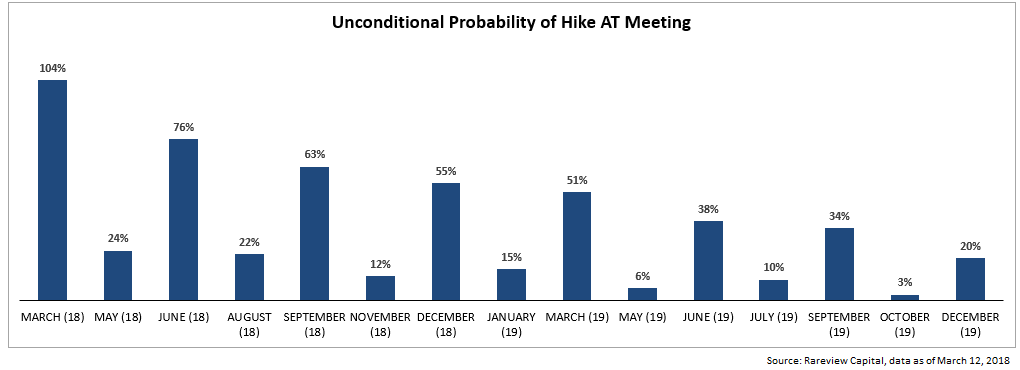

A Model Driven Approach To The Federal Reserve

The bar chart extrapolates the “unconditional probability” of an interest rate hike at a certain Fed meeting. Meaning, in isolation, what is the specific probability of a hike at each meeting?

Put another way, the model seeks to answer the question of once the outcome of March’s meeting is known, what is the probability the Fed hikes at the June meeting as well? Or, even September or December?

So, what is the model saying now?

Firstly, the unconditional probability of an interest rate hike at the March meeting is 104%, or “certain” of an interest rate hike at that meeting.

Secondly, the market is 76% “certain” the Fed will raise interest rates at the June FOMC meeting.

The unconditional probability of March and June have edged higher since the end of last year. Here is the math:

104% (March blue bar) + 76% (June blue bar) = 180% >>>> 180% / 2 meetings (March, June) = 90%, or “certain” of two interest hikes by June.

As a reference point, we view anything above 75% as extreme with 100 days of time value left in the interest rate market. Worded differently, there is no margin of error. Therefore, there is no more downside left betting on a March and June hike.

Looking past June, the market has priced in the probability, or risk, of the Federal Reserve raising interest rates 3 or 4 times between now and the end of the year, to pricing in the likelihood of hiking 4 times.

For example, our model illustrates that all 5 of the next quarterly FOMC meetings to March 2019 are priced with a greater than 50% probability of an interest rate hike at each meeting.

Therefore, if you want to make a bet on the path of Fed policy, the bet is either two or less hikes, or 5 or more hikes by March 2019. Again, there is no more downside on anything in between.

Otherwise, if by the end of the year, the Fed has hiked 3 or 4 times, then interest rates will be broadly unchanged from current yield levels.

Finally, as with any model, it is prudent to ask where the model breaks down or is wrong.

The answer is if the Fed were to hike at a non-quarterly meeting, known as an intra-meeting hike, or if they were to hike 50 bps at a quarterly meeting.

If an intra-meeting hike were to materialize it would lead the professional investment community to immediately shift quadrants to a “Measured Pace” from “Gradual Pace” like the hiking cycle between 2004 and 2006 under Fed Chair Alan Greenspan. There was a “measured” pace of a 25 bps interest rate hikes for 17 consecutive meetings.

The last time the Federal Reserve hiked interest rates more than 25 bps at a meeting was in the early 1990’s interest rate hiking cycle. There is no precedent for that in modern monetary policy.

What Does Rareview Capital Think?

Barring explosive growth that lifts the terminal rate embedded in the market from its current ~2.75%, we believe there are two likely outcomes this year for interest rate hikes.

Outcome 1: The Fed raises interest rates 4 times.

Outcome 2: The Fed raises interest rates 3 times.

If the Fed is going to raise interest rates 3 times this year, per their current forecast (i.e., “dot plot”), they will have to skip one meeting.

Because we are so late in the cycle, if the Fed does skip a meeting, the market will believe that they are done raising interest rates for this cycle regardless if the Fed’s “dots” call for 3 hikes this year.

In the meantime, because the market is priced for either 3 or 4 rate hikes this year, it will take at least until after the September FOMC meeting for the “certainty” of 4 hikes to be priced, if the Fed hikes at the next 3 meetings.

Yardstick #1 – Terminal Rate

The “terminal rate” is a “cyclical” concept.

Looking out to the end of 2019, investors are now faced with the choice of following “X hikes in X year” to “what rate is too much?”

The Fed’s prescribed terminal rate is 2.75%, which it appears from commentary from both San Francisco Fed President Williams and Chair Powell that regardless of the path to get there, that level is not changing.

The market is already priced for at least a 2.75% terminal rate. Meaning, every fixed income instrument longer than a 2-year duration now discounts that terminal rate.

Any professional forecaster calling for 8 hikes between now and the end of 2019 are explicitly saying that the terminal rate will be raised by 75 bps at some point this year. Here is the math:

1.5% current Fed Funds + eight 25 bps hikes = 3.5%, or 75 bps higher than 2.75% terminal rate in Fed’s dot plot

For portfolio construction, investors are asking what level the Federal funds rate – either realized or priced in the market – becomes a problem for equities and credit?

Specifically, investors are faced with deciding what terminal level in the intermediate-term is cheap enough to justify owning fixed income. Today, that level is between 2.75% and 3%. If you think there is a likelihood the Fed will raise the Fed Funds rates to 3.5%, then you would not want to buy today. Conversely, if you believe there is a likelihood the Fed does not hike to 3.5%, then you would want to own fixed income.

Our view is that the terminal rate is well below the 3.5% Federal Funds rate that many are now forecasting.

Yardstick #2 – Neutral Rate

The “neutral rate” is a “structural” concept.

Here is where we believe the neutral rate is for the cycle, or the point where Fed policy becomes “tight.”

Looking back over the last 35 years, with 100% accuracy in advance, we have found that the 5-year Treasury yield on the day of the first interest rate hike is the neutral Fed funds rate for the cycle.

In this case, that yield was 1.75% back in December 2015. The current Fed Funds rate is 1.5%. Meaning that the next rate hike – “certain” to be in March according to the market – will bring us to the neutral rate.

Combining what our model is telling us for future interest rate hikes – i.e., three this year and more next year – we can determine that the market is pricing enough interest rate hikes to bring the Fed Funds rate up to 2.75%, or at least 100 basis points beyond the neutral rate.

At that point, or near the September FOMC meeting, we believe the yield curve will have inverted, significantly increasing the chances for a market or financial accident.

Note, the interest rate forward market is already inverted beyond 2019, implying that after 2019, there is a better chance that the Fed will be easing policy. Worded differently, the inverted yield curve in the future is saying that this cycle is not different from previous ones regarding the neutral rate and the traditional yield curve that most monitor for an inversion will soon mirror the forward market. Remember, cash products roll into the forward market.

Realistically, we do not believe there is a high probability of more than 3 hikes this year. If so, it would likely follow a substantial move higher in the stock market, or even easier financial conditions seen in January 2018.

Conclusion

The market’s Mind Map is at the point of information overload. The asymmetry currently lies in walking back some of the upward pressure on interest rates now that the brain has become sensitized to all this information. After all, the 2yr, 5yr and 10yr yield are largely at the same levels for the last month, or longer.

The market is priced for 3 or 4 interest rate hikes in the front-end. Professional forecasters are calling for 8 hikes over the next two years. We know where we are wrong, either a shift in quadrants to a Measured from Gradual Pace or a 50 bps increase at a meeting.

We have identified inflection points regarding the two-key cyclical and structural yardsticks – terminal rate and neutral rate – historically relied on to measure when policy becomes too tight or we are nearing the end of the interest rate hiking cycle. We know the risk to the terminal rate, or pace of interest rate hikes, being adjusted higher is if the level of growth is stronger than 3%, inflation shows movement towards 2%, or the stock market has another year of extreme positive performance. Currently, that is not the case for any of the three inputs.

Our framework and process are laid out. We have a game plan for how to navigate the path of interest rates.

———————————

If you are interested in learning more about how we use our Federal Reserve model to potentially mitigate the risk of rising interest rates in your portfolio or for your clients, please call us at 203-539-6067 or email us at info@rareviewcapital.com.

Disclaimer

This material is for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any investment or any other security, including any investment with Rareview Capital LLC (“RVC”) or any of its affiliates or any other related investment advisory services. This material is not designed to cover every aspect of the relevant markets and is not intended to be used as a general guide to investing or as a source of any specific investment recommendation. This material does not constitute legal, tax, or investment advice, nor is it a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. In preparing this material, RVC has relied upon data supplied by third parties. RVC does not undertake any obligation to update the information contained herein in light of later circumstances or events. RVC does not represent the information herein is accurate, true or complete, makes no warranty, express or implied, regarding the information herein, and shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use. This material is subject to a more complete description and does not contain all of the information necessary to make any investment decision, including, but not limited to, the risks, fees and investment strategies of an investment. All investments carry a certain degree of risk, including the possible loss of principal. There is no assurance that an investment will provide positive performance over any period of time. There are specific risks that apply to investment strategies. Closed-end funds frequently trade at a discount to their net asset value. These risks should be reviewed carefully before taking any investment action. Since no one investment style or manager is suitable for all types of investors, this site is provided for informational purposes only. The statements contained herein are the opinions of RVC. This site contains no investment advice or recommendations. Individual investor results will vary. Rareview Capital LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Past performance is no guarantee of future results.