by Neil Azous, Chief Investment Officer

There are four potential ways to make money in municipal bond closed-end funds:

- Net-Asset-Value Appreciation

- High Income Distribution

- Broad discount-to-NAV tightening

- Discount-to-NAV capture (i.e., alpha generation)

Periodically, there is an opportunity to harvest two or three of those return streams at the same time. However, it is extraordinarily rare that all are aligned simultaneously, especially to this degree. We provide details below.

- Net-Asset-Value Appreciation: The cash municipal bond market has started to recover. However, there is still significant scope for further price appreciation. For example, the lower-rated segment of the tax-exempt municipal market remains down between 2% to 6% from their pre-COVID-19 returns. Most recently, the lower-rated tranches have appreciated the most. We attribute this to a greater belief by investors in the Government programs enacted to support the municipal bond market. Said differently, investors are beginning to believe the Government significantly reduced the left-tail risk of municipalities not being able to access the capital markets for new issuance. Based on the positive reception in the corporate credit markets to government support, we believe a similar sentiment will become more entrenched soon in the municipal bond market. The catalyst for that may be the next round of fiscal stimulus which is expected to provide a large aid package for states. Finally, we believe a unified Democratic Administration and Congress would more robustly support the states, which may increase the value of municipal bonds.

-

- Important Sidebar: The higher yields of lower-rated investment-grade municipal bonds now offer a potential cushion against higher interest rates, which is not the historical norm. For example, single-A or triple-B tax-exempt municipal bonds typically trade equal-or-slightly above US Treasury yields. Currently, they trade at 100-250 basis points more than US Treasury yields, depending upon the maturity. What that means is that a portfolio of tax-exempt municipal bonds with an average credit rating of single-A would have a neutral excess return should interest rates rise by 100 bps or more. Conversely, if the yield spread between lower-rated municipal bonds and US Treasuries narrows, then there will be a pleasant, positive excess return.

- Important Sidebar: The higher yields of lower-rated investment-grade municipal bonds now offer a potential cushion against higher interest rates, which is not the historical norm. For example, single-A or triple-B tax-exempt municipal bonds typically trade equal-or-slightly above US Treasury yields. Currently, they trade at 100-250 basis points more than US Treasury yields, depending upon the maturity. What that means is that a portfolio of tax-exempt municipal bonds with an average credit rating of single-A would have a neutral excess return should interest rates rise by 100 bps or more. Conversely, if the yield spread between lower-rated municipal bonds and US Treasuries narrows, then there will be a pleasant, positive excess return.

- High Income Distribution: Closed-end funds generally use a moderate amount of leverage to acquire more assets to pay higher distribution yields. Since May, there have been two rounds of distribution rate increases in the municipal bond closed-end fund sector. As a yardstick, the sector yield has risen to ~5% relative to ~5.7% historically. We expect distribution rates to climb back to their long-term average, especially if the yield curve steepens.

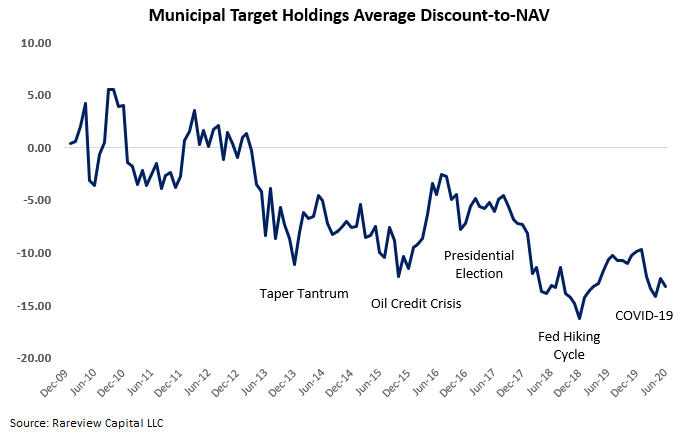

- Broad Discount-to-NAV Tightening: When the Fed cut interest rates to the Effective Lower Bound (ELB), they created a significant tailwind for fixed income closed-end funds because their financing costs dropped materially. Mechanically, those cost savings are passed to shareholders in the form of higher distribution yields. That typically results in the discount-to-NAV tightening as the relative yield between a closed-end fund and traditional cash fixed income product widens. Discounts in the municipal bond closed-end fund universe remain in the top 10% of history. We believe discounts will narrow because leverage costs are significantly lower, and the Federal Reserve is expected to hold interest rates at the ELB until the end of 2022. Also, following the astounding amount of liquidity injected into the system, if there is a V-shaped economic recovery that includes additional support for states in the next stimulus package, there is scope for this sector to trade at a premium once headline risk dissipates.

CEF - Discount-to-NAV Capture: Currently, the potential to capture narrowing in the discount-to-NAV in fixed income closed-end funds is opportunistic – the pandemic created severe dislocations across asset classes. The absolute and relative historic level of discounts remains very wide. At Rareview Capital, we have a model-driven approach to capturing the changeover in the discount-to-NAV. We believe that the potential discount-to-NAV capture over time can increase total returns. Importantly, we can demonstrate this “alpha generation” in a positive or negative market environment, which is how active management should be measured.

While municipal bond closed-end funds had strong absolute performance in 2019, discounts-to-NAV’s never had the opportunity to fully tighten after the 2017-2018 interest rate hiking cycle that resulted in historic discount widening. And, just as that discount narrowing was set to potentially materialize this year, COVID-19 reversed the trajectory.

The key point here is that you are being given a second opportunity at that same playbook. The difference this time is that there are more line items in the “sum-of-the-parts” equation. Also, many of these inputs are at an extreme or provide a high degree of cushion. Collectively, we believe municipal bond closed-end funds could generate well-above-average total returns.

+ Interest rates projected to remain at Effective Lower Bound (ELB) until at least the end of 2022

+ Cash municipal bonds have a large cushion against higher interest rates

+ Cash municipal bond market backstopped by government authorities > Additional state support forthcoming

+ Lower leverage costs > higher distribution rates > narrower discount-to-NAV’s

+ Closed-end funds have high earnings coverage ratio (i.e., ~105% and growing)

+ Opportunistic discount-to-NAV entry point level (i.e., -11%)

+ Potential discount-to-NAV-capture opportunity (i.e., alpha generation)

_____________________________________________________________________________________________

= potentially well-above-average total returns

If you are interested in learning more about how we use closed-end funds to construct portfolios in separately managed accounts (SMA), including our Managed Municipal Bond (Tax-Exempt Income) strategy, please call us at 203-539-6067 or email us at info@rareviewcapital.com.

Disclaimer

This material is for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any investment or any other security, including any investment with Rareview Capital LLC (“RVC”) or any of its affiliates or any other related investment advisory services. This material is not designed to cover every aspect of the relevant markets and is not intended to be used as a general guide to investing or as a source of any specific investment recommendation. This material does not constitute legal, tax, or investment advice, nor is it a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. In preparing this material, RVC has relied upon data supplied by third parties. RVC does not undertake any obligation to update the information contained herein in light of later circumstances or events. RVC does not represent the information herein is accurate, true or complete, makes no warranty, express or implied, regarding the information herein, and shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use. This material is subject to a more complete description and does not contain all of the information necessary to make any investment decision, including, but not limited to, the risks, fees and investment strategies of an investment. All investments carry a certain degree of risk, including the possible loss of principal. There is no assurance that an investment will provide positive performance over any period of time. There are specific risks that apply to investment strategies. Closed-end funds frequently trade at a discount to their net asset value. These risks should be reviewed carefully before taking any investment action. Since no one investment style or manager is suitable for all types of investors, this site is provided for informational purposes only. The statements contained herein are the opinions of RVC. This site contains no investment advice or recommendations. Individual investor results will vary. Rareview Capital LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Past performance is no guarantee of future results.

Other important risk considerations, products or terminology:

- Closed-End Fund Leverage: Leverage is a speculative technique that exposes a closed-end fund to greater risk and increased costs than if it were not used. The use o leverage may cause greater volatility in the level of a closed-end fund’s NAV, market price and distributions on its Common Shares. Leverage will also result in higher fees due to the closed-end fund manager because the amount of assets under management will be included in the closed-end funds Managed Assets. There can be no assurance that a closed-end fund will use leverage or that its levered strategy will be successful during any period in which it is employed. Additional information on how closed-end funds use leverage can be found at CEF Connect.

- Tax Risk: New federal or state governmental action could adversely affect the tax-exempt status of securities held by a closed-end fund, resulting in higher tax liability for shareholders and potentially hurting performance as well. It is strongly suggested that investors obtain independent advice in relation to any investment, financial, legal, tax, accounting or regulatory issues discussed in this commentary.

- Net Asset Value (NAV): A mutual fund’s price per share or exchange-traded fund’s (ETF) per-share value. In both cases, the per-share dollar amount of the fund is calculated by dividing the total value of all securities in its portfolio, less any liabilities, by the number of fund shares outstanding.

- Discount-to-NAV: A pricing situation that occurs with a closed-end fund when its market price is currently lower than the net asset value of its components.

- Alpha: We determine Alpha as the relative return of a Closed-End Fund’s (CEF) share price to its Net Asset Value (NAV). Any return of the share price that is greater than the NAV is deemed to be positive alpha. Any return that is negative than the NAV is deemed to be negative alpha.

- Basis Points (BPS): One hundredth of one percent, used chiefly in expressing differences of interest rates.